Ethos Life Insurance Platform¶

Watch Ethos Life Insurance Platform VIDEO

Ethos Life Insurance is a digital agency founded in 2016 that simplifies life insurance by offering no-medical-exam policies with instant approval and same-day coverage for eligible applicants. Headquartered in Austin, Texas, and publicly traded on Nasdaq since January 29, 2026, Ethos acts as a broker connecting customers with established carriers like Legal & General America, Ameritas, TruStage, and Protective.

The company offers three primary policy types tailored to different needs:

Term Life: Available to ages 20–69, with coverage up to $3 million (for ages 20–50) or $500,000 (for ages 51–85) and terms of 10, 15, 20, or 30 years. Whole Life: A permanent policy for seniors (ages 66–85) offering guaranteed approval with benefits ranging from $1,000 to $30,000. Guaranteed Issue Whole Life: Designed as final expense coverage for ages 45–85, providing $5,000 to $25,000 in coverage with a graded death benefit if death occurs within the first two years. Key features include free estate planning tools (wills and trusts), a 30-day money-back guarantee, and competitive rates for smokers and older adults, though premiums may be higher than average compared to fully underwritten policies due to the lack of medical exams.

- Ethos Field Underwriting Guide

- Ethos Agent Portal

- Sample Agent Public Site (Michael's)

- Folder of PDFs in Proton Drive

Our Ethos Account Manager¶

- Ryan Schuhmann

- ryan.schuhmann@getethos.com

- 415-237-2001

- Appointment scheduler

Term Life Options¶

- Term Length: 10, 15, 20, 25, 30, 35, 40

- Face Amount: $50,000 - $2M

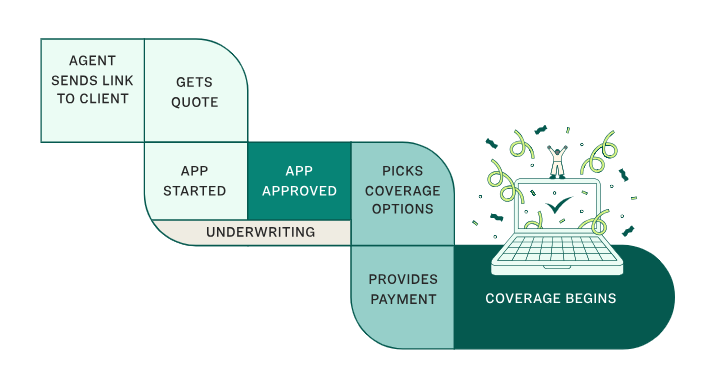

The Process¶

Life Insurance Carriers¶

Tabs¶

Lincoln¶

- Works with iPipeline

- Agent Portal

- Case manager email: termacceluwnb@lfg.com

American General (AIG)¶

- Works with iPipeline

- Agent portal: Connext

- Phone: 800-631-5777

- IP Agency #:

Q180 - AIG Term Life Quoter

Transamerica¶

- Works with iPipeline

- Producer Portaltransact.transamerica.com)

United Farm Family¶

Best used for End-of-Life / Burial Insurance - Works with iPipeline - Producer Portal

¶

Running Quotes, Applications, Hints & Tips¶

Unusual Health Issues¶

- For issues such as diabetes, cancer etc, use the Docusign template

[L-IP-01] Life Insurance Quote Requestto have IP run the detailed quote for you. - For diabetes: The largest factor on a client’s rating here, and premium possibilities, will be how well their diabetes is managed. Before I can run an accurate illustration and review the viability of the case we should gather as much underwriting information as possible. I’ve attached a copy of our diabetes questionnaire. Once completed, please return it to me and from there I can obtain rating estimates. Use this DocuSign template

[L-IP-02]_Life_Insurance_Diabetic_Questionaire-v1.

Cigar Smoking¶

Lincoln and Prudential are the laxest for vaping and occasional smoking.

Typical Industry-Standard View on Cigar Smokers¶

This policy will apply only to occasional cigar users and not other forms of tobacco. Based on current mortality information, underwriting will consider cigar use a non-factor in the risk evaluation process if: 1. The use is admitted at the time of application/inquiry and all case data coincides with the admitted degree of usage; and 1. No more than one cigar per week; and 1. No nicotine metabolites (cotinine) are present in the urinalysis done for AGL/US Life or any other company within the past 12 months; and 1. There is no use of tobacco products other than occasional cigars for at least 5 years prior to the time of application or inquiry.

iPipeline¶

Gain Access to the iPipeline Platform¶

- Visit IPFinancialServicesLLC.com

- Click on

Product Quotes/Illustrations. This will take you to iPipline. - At the login screen, click

Create an account. - Enter your information. You must use your Innovation Partners email address.

- A request will then be sent to the back office for processing.

- If you have any issues with the process, please email John Kyger at IP.

Using iPipeline¶

When running a life insurance quote, I use iPipeLine, run the quote, and then down the ListView then highlight it and share with my client.

Delivering the Policy¶

How best to deliver other-than-applied-for policies¶

Sometimes policies don’t get issued as applied for, such as when a client gets rated, or the premium comes back lower than expected. Successfully delivering these policies can make or break your bottom line. It has often been said that the difference between making it and breaking it in our business is the ability to place cases that are approved “Other than Applied For.”

How to Deliver a Rated Case¶

-

Present it as good news…be sure you present it in just that way. “I have some GOOD NEWS about your life insurance application…the company has made an offer!”

-

Be prepared with an option that costs them LESS. Not that you will always sell it, but be prepared with an offer that will actually cost your client LESS than they were considering. If they were applying for $500,000 of 20 year term and move from Preferred to Standard, maybe you need to be ready with $300,000 for 10 or 15 years to get to a premium level that is less than what they were considering. You must give them options and having one that is less premium builds huge credibility.

-

Have some passion. Here’s a fact: of all the people you work with, these are the people that need our product the most. Our health is either getting better or getting worse. If your client’s health gets better you will get them a better rate; if it gets worse, this becomes the best offer they ever received. They win both ways. These families need this protection more than any others you work with. It is urgent and important that they accept this offer and put the policy in force.