Derivatives¶

“Derivatives are financial waepons of mass destruction.” ―Warren Buffett

Hedge Funds¶

“A number of smart people are involved in running hedge funds. But to a great extent their efforts are self-neutralizing, and their IQ will not overcome the costs they impose on investors.” ―Warren Buffett

Ask Nick...¶

This is from NMI July, 2001.

QUESTION FROM AN ADVISOR¶

I have a question regarding the use of hedge funds as an asset class. Is there a place for a hedge component in a well-diversified stock fund portfolio? My accounts are 100% equities (large-cap value, large-cap growth, and international) with a high degree of diversification. Should I consider putting 10% of my clients' portfolios in an actively managed fund that invests in hedge funds? In the long term, would it increase return and reduce volatility? Could it retain return while reducing short-term volatility?

NICK MURRAY'S ANSWER¶

I think there's something in the best of us whereby, when we have finally achieved enough wisdom to craft superbly diversified equity portfolios for our clients and now need only leave them alone to do their glorious work, we find ourselves unable to leave them alone. Your inquiry is, I believe, prompted by this impulse.

Let me make a few general observations, in no particular order of importance. (1) Hedge funds are not an asset class; they're a management style – or rather, a mixed bag of highly idiosyncratic management styles, as wildly disparate as hedge fund managers themselves. (2) Hedging is a high-reward, high-risk management style; neither it nor any management style can provide meaningfully higher long-term returns without concomitantly increased risk. The notion that a hedge fund, much less a whole basket of hedge funds, could provide meaningful melioration of short-term volatility is (a) an absurdity on its face and (b) irrelevant, as all short-term issues are irrelevant. (3) The cost structure of a fund of hedge funds – involving two layers of asset management fees plus your compensation (however it may be buried) – could not fail to destroy the ultimately illusory incremental return. (4) The fundamental notion that changing the character of 10% of your portfolios would meaningfully alter their long-term returns or volatility is mathematically improbable in the extreme.

The fundamental issue here, if you will permit me to say so, isn't hedging at all, but the deep need in us to try to be heroes for our clients. (However misguided, this is always laudable.) I would invite you to snap out of it, and observe (a) that your clients don't need you to be a hero; they need you to help them achieve their goals, which you are so clearly doing, and (b) that you are already a hero for the ages, because you already have your clients' long-term capital entirely in equities, which not one advisor in a hundred ever achieves.

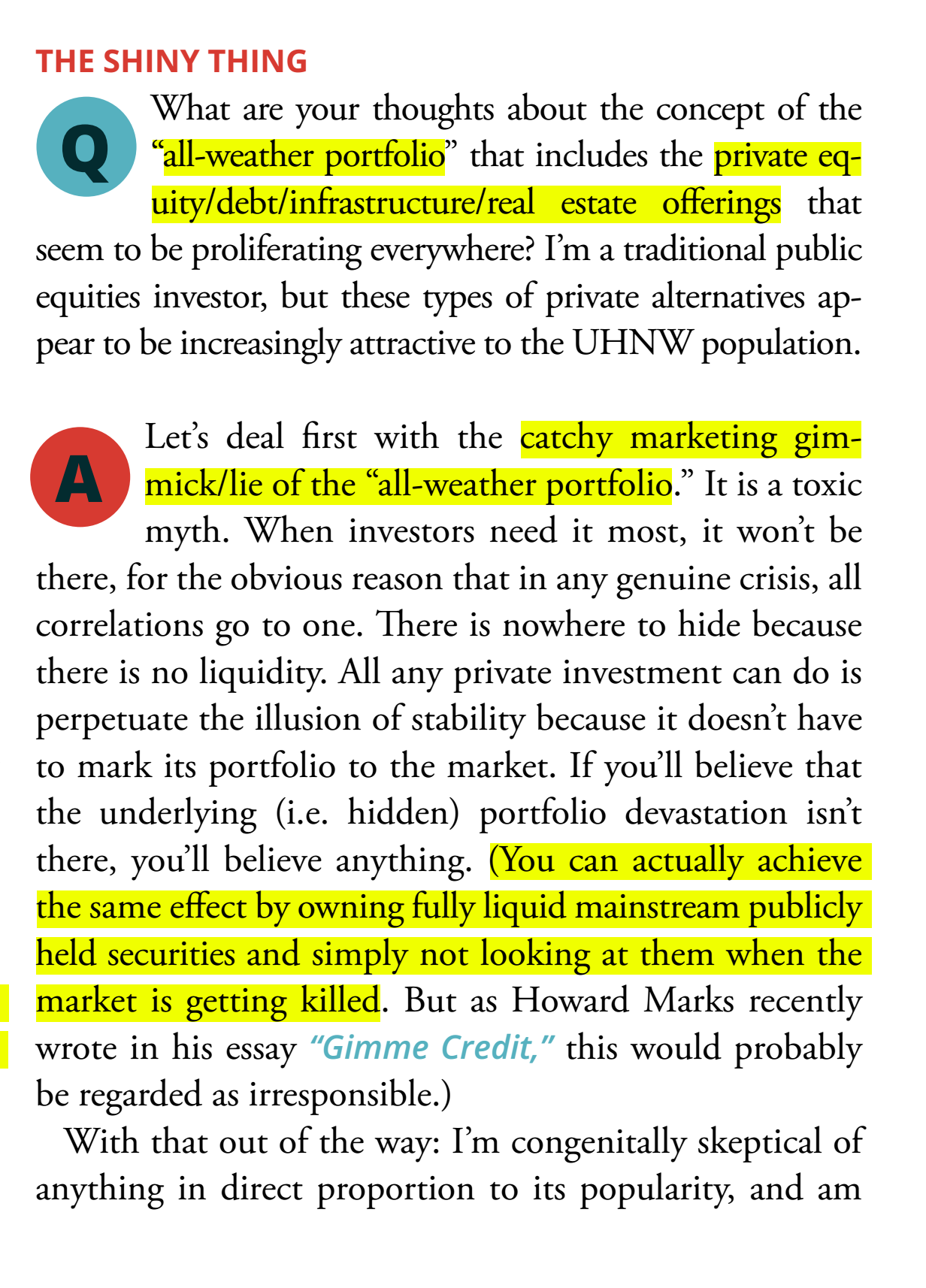

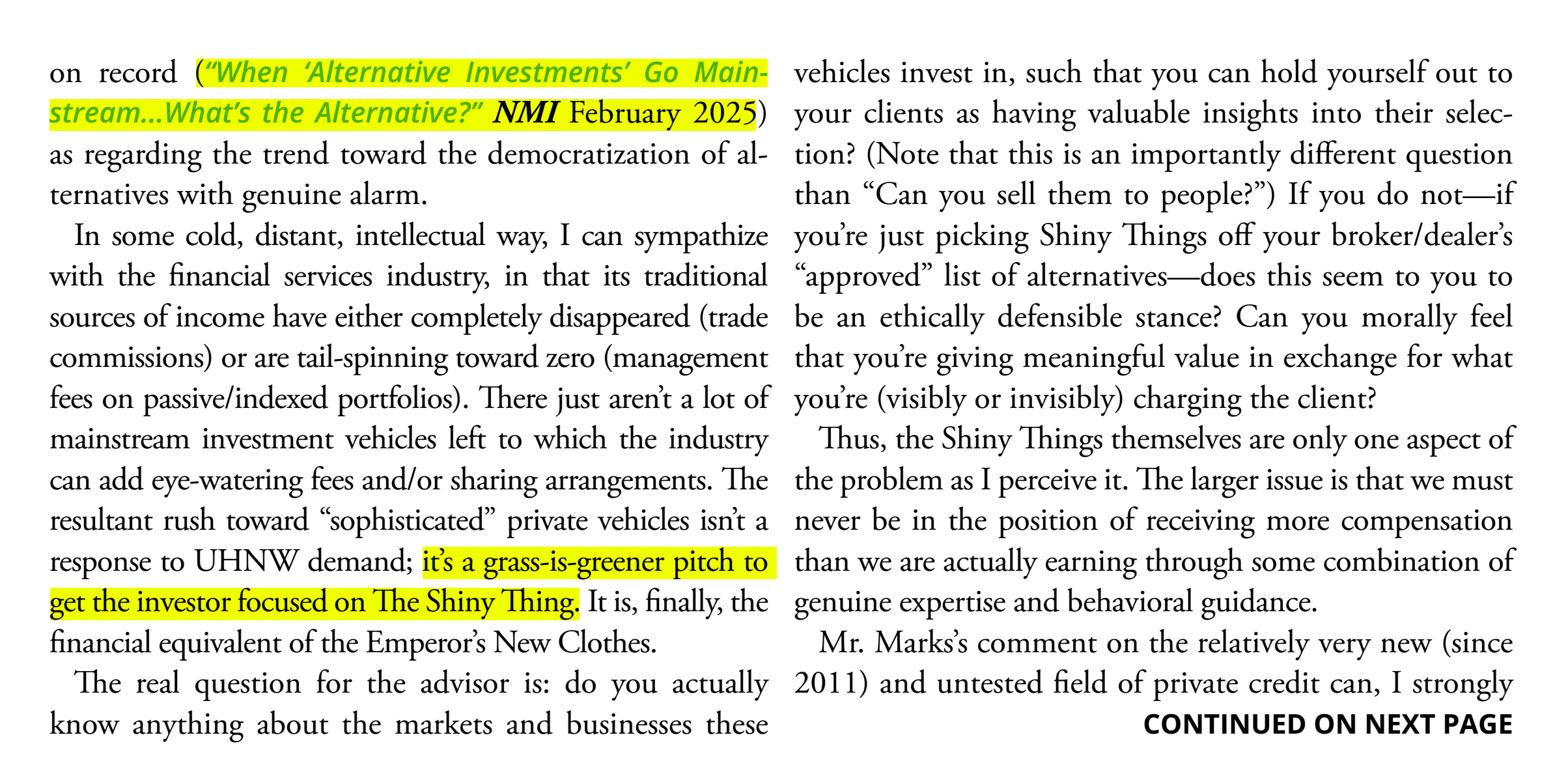

All-Weather Fund¶

(Private Equity/debt/infrastructure/real estate)

Alternative Investments¶

Stock Futures and Options¶

“Warren Buffett thinks that stock futures and options ought to be outlawed, and I agree with him.” ―Peter Lynch

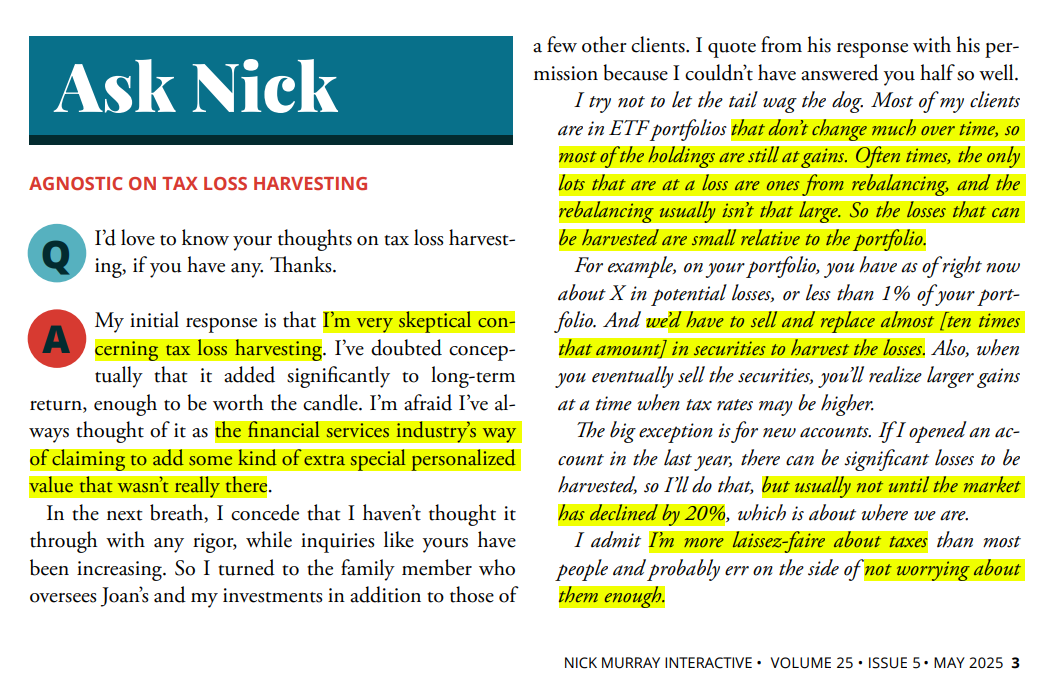

Tax Harvesting¶