Compliance is operating within the guidelines of the licenses you hold. We're building something great - not something that's going to last just a few years and fade away. This is something that will be around long after we're gone - a business that will be there for our children, and our children's children.

If you're serious about building your future, you have to expand your vision beyond the "here and now." You have to look years down the road and make decisions today that will assure the survival of your business long-term. With ownership you're more than building a business, you're building a legacy that may last for generations to come. That's why compliance matters. Compliance means business protection. That means keeping watch over your business to make sure nothing happens that could jeopardize your future. Our opportunity is too great to allow any individual or group to damage our credibility, our reputation or our integrity.

Note: the compliance topics below are copied from correspondence via IP and may be out of date.

Social Media Websites/Sites¶

9/8/2021

As the regulatory oversight of social media and other communication with the public comes under heightened scrutiny, it is imperative that all representatives are vigilant about how they communicate through social media and other mediums. Adhering to the firms policies and procedures minimizes the risk to yourself, the firm and your clients. Please adhere to the companies policies and procedures where social media is concerned.

It has been noted that a number of representatives have been using social media sites to post profiles, that include the fact that they are registered representatives or investment advisor representatives with IPLLC. Per FINRA, social media sites are deemed to be advertisements and therefore special monitoring, archiving and approval of the sites is required.

Below is IPLLC’s requirement to maintain the social media sites:

-

If you have a website or are listed on a social media site such as LinkedIn.com, Facebook.com, X.com or other social media platforms, you must submit your social profiles and/or website(s) to IPLLC compliance at compliance@innovationpartnersllc.com for review and approval.

-

Advertising Rules apply to all websites. All websites must be sent to FINRA for approval. All fees must be paid before websites will be submitted to FINRA. Broadridge Forefield is our advertising provider. Please refer to the advertising notification and email to address any advertising procedural requests and requirements.

-

Sign up with Global Relay for the monitoring of your social media website. You will receive a separate email from GLOBAL RELAY, with instructions regarding the submission of your website and social media information.

FINRA and other Industry Regulators examination priorities focus on outside business activities to include information retrieved from social media websites. IPLLC’s focus is to ensure that all representatives are compliant with the regulatory requirements. IPLLC is required to conduct constant social media searches for materials being posted by representatives associated with the firm.

Note: You will not be allowed to maintain any social media pages or websites, if the above procedures are outstanding. You will be required to remove your website pages, if the compliance procedures are not completed.

Our position on no-sales-charge (NAV) mutual fund trades.¶

Your "discount" is your commission.

With some fund companies, a Registered Rep could write his own sale, or those of a family member, and avoid the A-share sales charge. If you were to bypass the sales charge, no one gets paid. Not you. Not your manager. Not even IP. It is contrary to the our business philosophy, and it's bad for your business.

We don't charge our clients more than we charge ourselves. I believe there should be no "wholesale" / "retail" pricing distinction in our business. We are all clients and should pay the same as non-Rep clients do. It is very powerful to be able to make this statement to your clients (and downlines!).

If price is the issue, then price isn't the issue. Why do you feel the need to give a discount to the client? Is the client asking for it, or are you leading with the discount?

Most importantly, by giving a discount to yourself and family you are not living the philosophy of "do unto others as thyself". There is tremendous leverage when you can tell a client that you pay the same costs as they do.

"Mr. Client, I realize that this upfront expense seems like a lot, however this is what it takes to get the finest investment company to manage your money for you. Every client pays it, even I had to pay it . Just because I represent them, doesn't mean I get a discount, but I so believe in their ability that I gladly paid it."

Use of the term "Financial Advisor".¶

When you hold a Series 65/66 license then you can call yourself a Financial Advisor. With merely a Series 6/7 you are a Registered Rep.

Fund Suitability & Risk Questionnaire¶

Read Nick's ATY 169 June 18 - The Vexing Issue of the Risk Tolerance Questionnaires PDF

Read Nick's ATY 170 June 19 - Limits of Your Responsibility PDF

Non-Licensed Assistant¶

-

It is possible to register a non-licensed person with FINRA who can help with client service. There is $25 monthly fee and includes a company email address.

-

If you're going to hire an assistant, make sure he/she is older and more responsible than you.

-

You can have an assistant, spouse, partner, adult child, etc registered with FINRA as a non-licensed Assistant.

-

This will allow him or her to talk to clients to help with paperwork or answer non-product questions.

-

All he/she has to do is get fingerprinted:

-

Go to www.brokerFP.com to find a location and schedule an appointment.

-

Fingerprints will cost the applicant $17.50 paid directly to the fingerprinting service.

-

IP's fieldprint code: ???.

-

For "employer" write: ???

-

After getting fingerprinted, send an email to ??? informing her about that the fingerprinting was completed and to which Advisor the Assistant is "attached".

-

The Advisor will be billed $25 per month (not the Assistant).

The duties of an assistant can be varied, mostly depending upon what the Advisor needs him/her help with. But some of the more common ones include:

-

Paperwork.

-

Following up with prospects, clients and downline Advisors. You can give American Funds permission to ask questions about clients accounts, on your behalf.

-

Staying abreast of what's happening in IP / AdvisorFirst Group and helping the Advisor digest it.

-

Learning new procedures and helping the Advisor learn them.

-

Writing life insurance and living trust business.

Accepting Cash¶

You are PROHIBITED from accepting the following from your clients: - CASH - MONEY ORDERS, in some cases a client can add money to an existing account via a money order. - CASHIERS CHECKS, in some cases a client can add money to an existing account via a cashier check. - TRAVELERS CHECKS

Customers must have a U.S. checking account for writing checks or a savings account for automatic drafts in order to make securities purchases.

Any attempt to pay for a securities transaction with cash or non-traceable cash equivalents must be reported to the Compliance Department immediately. If you suspect that this occurrence is imminent, you must notify the Compliance Department immediately. In the event that you discover currency has been received or involved in a transaction, it must be reported to the Compliance Department immediately.

Paying Clients for Referrals¶

You can pay clients for referrals just as if you were to buy leads through an lead generating service. But, you must buy every single "lead". The payment for the lead must be fixed and can obviously not be contingent on a sale or in any way price determined by a sale.

So for example, you could pay $50 for every single lead referred to at the time the referral data is provided. You can not just pay the referring person if a client calls and opens an account but then not pay when the client doesn't open an account; that would be paying a referral fee contingent on a sale which is prohibited. Obviously the risk is that the leads are bad and you don't bring on any new clients from it, but that is the risk with buying any type of lead and obviously you wouldn't continue to buy bad leads after a while.

Giving and Receiving Gifts¶

What You Can, and Cannot, Give & Receive

The prohibitions in Rule 3060 generally do not apply to personal gifts such as a wedding gift or a congratulatory gift for the birth of a child, provided that these gifts are not “in relation to the business of the employer of the recipient.” In determining whether a gift is “in relation to the business of the employer of the recipient,” members should consider a number of factors, including the nature of any pre-existing personal or family relationship between the person giving the gift and the recipient, and whether the registered representative paid for the gift.

When a firm bears the cost of a gift, either directly or by reimbursing an employee, FINRA presumes that such gift is in relation to the business of the employer of the recipient. The analysis of whether a gift is “in relation to the business of the employer” is required in connection with all gifts; firms should not treat gifts given during the holiday season or for other life events as personal in nature.

-

You can give and receive gifts of any value from someone who is not a client.

-

You can give and receive gifts of any value from a client so long as they do not have a relationship with you as an RR through their employer (such as a wholesaler).

-

You cannot give nor receive gifts in excess of $100 in value in a year from anyone who has a relationship with you as an RR through their employer.

Presenting the Prospectus¶

Every time you do business with a client you must present them with a prospectus. You can email the PDF to them, or share the link with them. For American Funds you can find it under the "Resources" section of each fund.

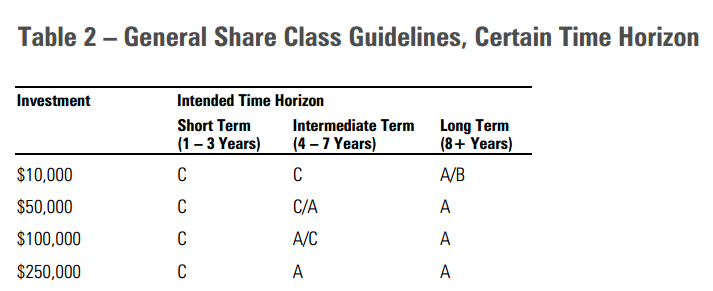

Share Classes Suitability¶

Watch AF MKOM 1667 - A-Shares vs C-Shares vs F-Shares VIDEO

A-Shares vs C-Share Suitability¶

Recently, the SEC and FINRA have tackled the topic of share class suitability. The two regulatory bodies have shown concern that investors are being overcharged by brokers who have directed clients to C share classes rather than realizing breakpoint discounts with A shares. FINRA has conducted numerous “sweeps” of brokerage firms looking for these sales abuses, and has issued more than $50 million in fines and investor restitution since 2003.

-

A-shares have up-front sales charge (UFSC) but the lowest annual expense. The up-front sales charge is reduced by investing larger amounts within a 13-month period (called "breakpoints"). It's a one-time fee, then a very low-cost forever. The UFSC pays for two things: high quality active management, and a professional coach (you).

-

C-shares (and F-shares) have no up-front sales charge but a higher annual expense, which stays constant throughout the lifetime of the account (exception: American Funds reduces the annual expense after 8 years to that of an A-share). There is also a 1% contingent deferred sales charge (CDSC) for one year.

-

For investors who are extremely confident that their time horizon will be less than five years, and the investment amount is less than $500,000, then C shares aare the better option ("5 and 5").

Two factors must be considered when evaluating the appropriate share class for an investor

-

The investor’s investment amount.

-

Time horizon.

As stated above, C-shares tend to cost more for a client than A-shares, thus the use of C-shares needs to be properly defended. Here are some tips:

-

"I can provide better long-term service with C-shares because my compensation is spread over a longer time frame, than with an A-share in which the compensation is mostly upfront" is not a valid argument with FINRA. They expect Registered Reps to provide the same level of services regardless of the compensation method.

-

Valid: the client may want to withdraw or move the money to another account within 1 - 5 years. Such as a variable annuity or fee-based account.

-

Valid: the client insists that they are adverse to the upfront sales charge of A-shares. They want all their funds invested in the market immediately.

-

Note: if you are investing in American Funds C-shares make sure to mention that after 8 years the annual expense reduces.

Understanding American Funds A-Share Breakpoints¶

Vist the AF Master Spreadsheet: Commission Calculator to see the individual breakpoint schedule for American Funds.

-

All immediate family members' accounts count in aggregate to reach the breakpoints.

-

Children under age of 21 count towards the family breakpoint - and their account benefits from the higher breakpoint as well. Once they turn 21 they no longer count towards the aggregate. Note: AMF does not do an automatics sweep of all accounts, so your clients may benefit from the reduced up-front sales charge for a longer time. Make sure to inform your client that that is not guaranateed.

-

When adding new money to an existing account, it is the combined value of all accounts or their total depostis (minus withdrawals), whichever is greater, that counts toward reaching a breakpoint.

-

At $1M there is no upfront sales charge, but the is a 1% CDSC for 18 months.

Client has an existing American Funds account of $50k in C-shares. You open another account for the same client for $60k A-shares. Which breakpoint does the new $60k qualify for?¶

- $100k. C and A-share count together.

-

$50k. C and A-share don't count together.

-

Answer: 1

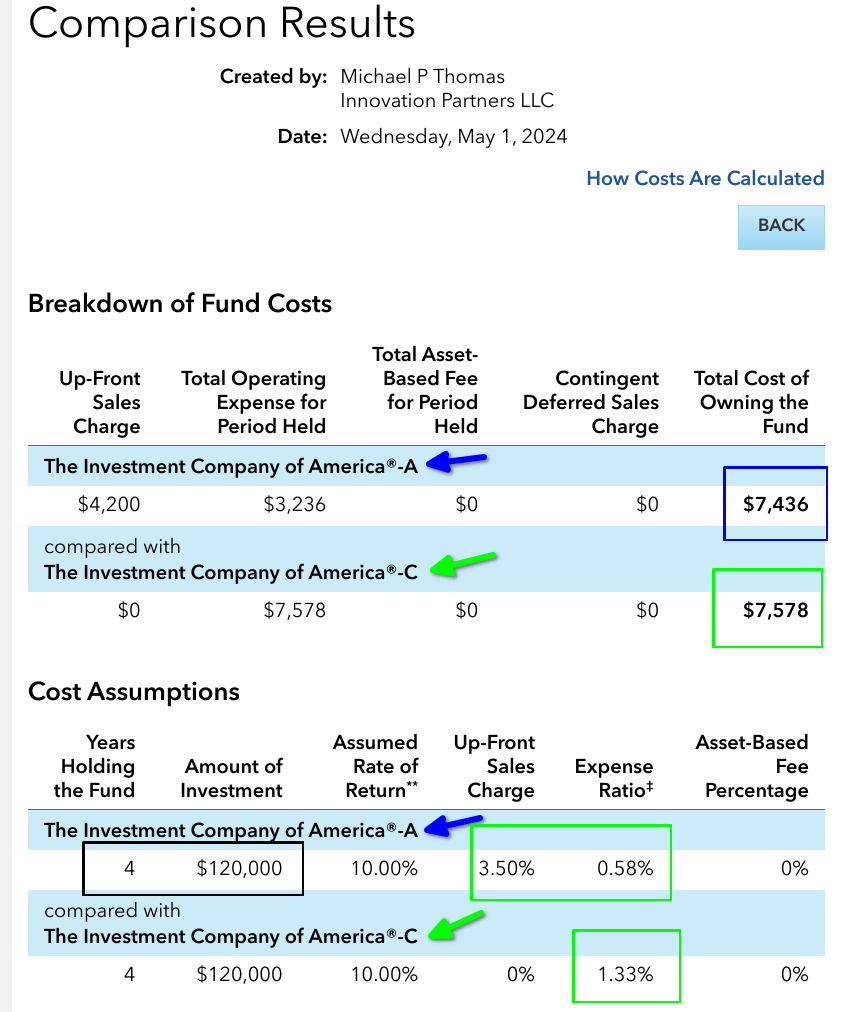

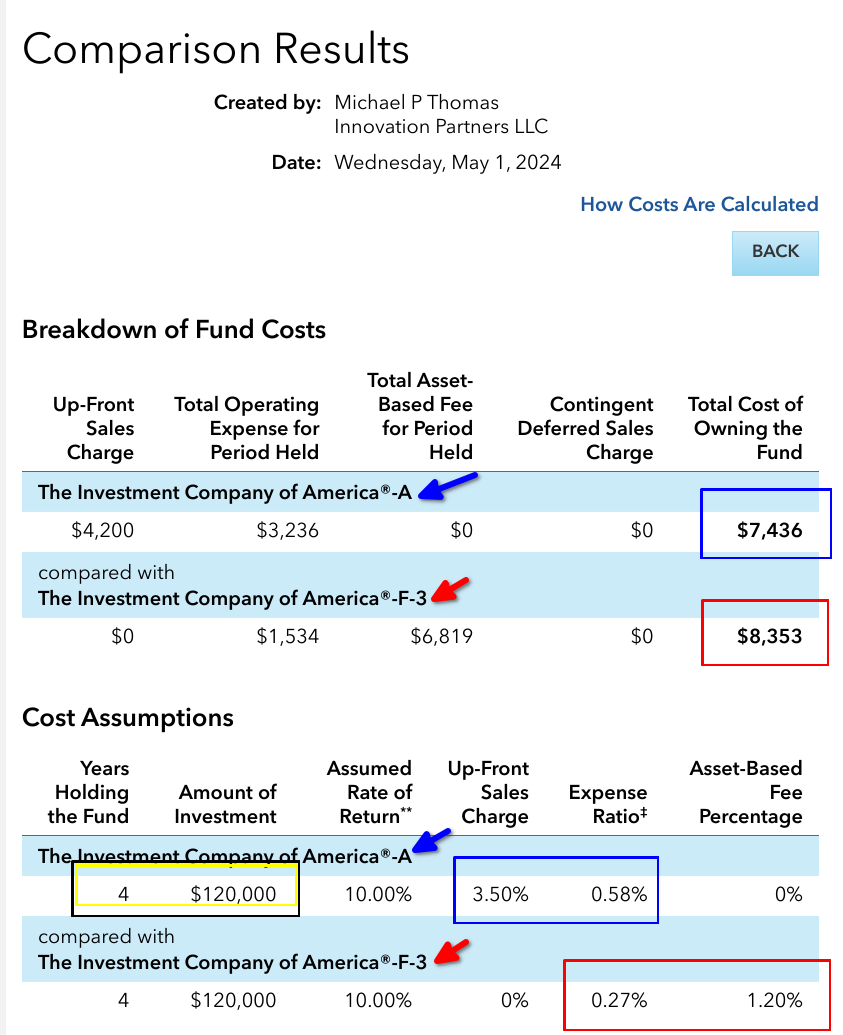

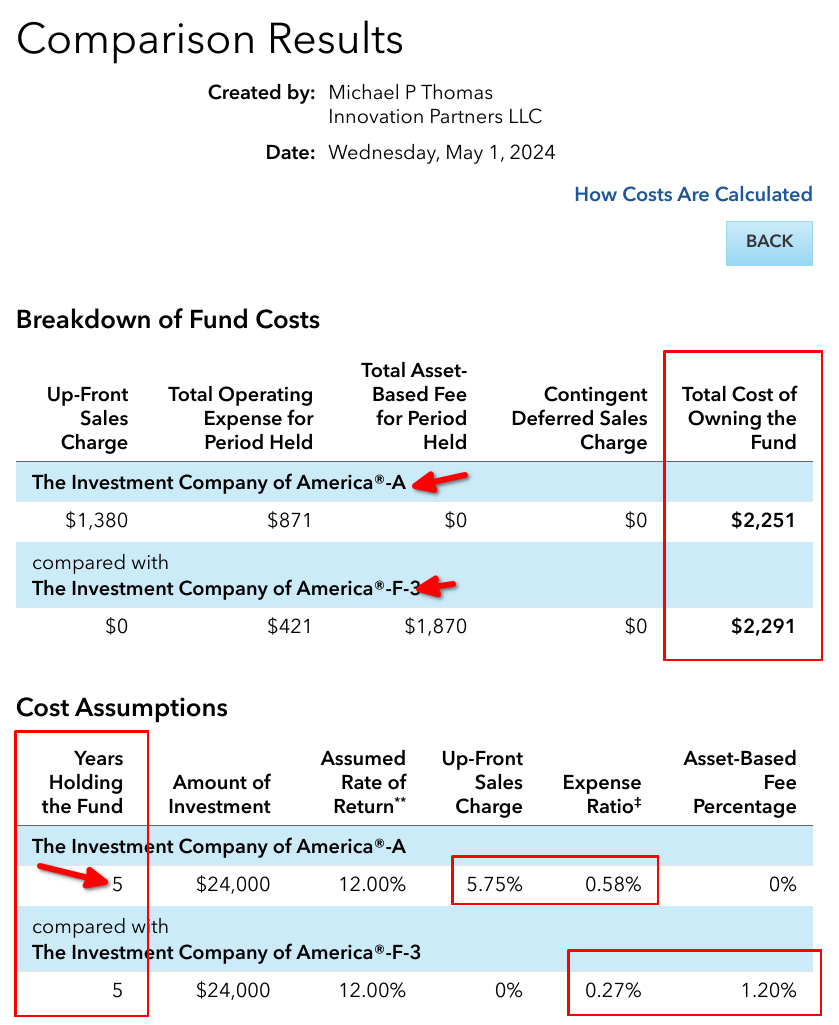

Comparing A-Shares vs C-Shares vs F-Shares¶

"My underlying philosophy on share classes (and B/D vs Advisory) is: if the investment is the same, and the Advisor is the same, then fees are important, and thus the Advisor should select the class that is the most inexpensive for the client. Remember, the cost is never just the raw cost itself - it's what the additional cost would have grown into had it stayed in the investment." -Michael

For more details on Advisory/Fee-Based business visit AFW S.7.

The Two Best Tools for Determining the Best Share Class for the Clinet¶

- American Funds Share Class Cost Comparison Calculator.

- Run a hypotherical illustration of actual mutual funds with all the share classes. If you're ever in doubt - run a hypo!

A vs C vs F¶

Watch MKOM 1607: A-Shares vs C-Shares vs F-Shares YOUTUBE VIDEO

- Note: I used F3 shares as they are the cheapest of F1, F2 & F3.

A vs C. $120,000 (this was used with an actual client)

A vs F. $120,000 (this was used with an actual client)

A vs F. $24,000 (this compares the most expensive version of an A-share and the cheapest version of F shares.)

Further Research on Share Classes¶

-

Please read Nick Murray's article "Explaining Fees" on page 83 of the Nick Murray Reader Audiobookshelf PDF

-

Read the Compensation page AFW M.3

-

Read the objection Load vs No-Load AFW S.12.1

Client Requests Account Liquidation¶

Customer account liquidation requests must be handled with the utmost care.

-

Ensure that you receive the request in writing (either by mail, email to include the required third-party account documents etc.)

-

Ensure that you provide the client with information of how the liquidation will affect the account.

-

Provide information regarding fees, and surrender charges, administrative fees and any other fee associated with the liquidation to the client (most of these fees would have been documented upfront and prior to purchase of any securities product)

-

Keep written notes/records of all phone conversations with the client (date and time of call, comments and transcript of discussion, recommendations, documents discussed, title and document number of educational materials and company name). Clients concerns etc.

-

Inquire about any issues that the client may be having financially, or if there were any changes to economic status, family etc. that would have caused the full or partial liquidation of an account

-

Make note of all responses regarding the clients financial situation.

-

Our account administration and compliance department will request information regarding the liquidation and as such all representatives must provide documents upon request.