title: Variable Annuities description: [AFW S.6] Protecting the Golden Eggs from the Golden Goose. published: true date: 2026-06-30T08:07:58.666Z tags: editor: markdown dateCreated: 2021-04-20T07:30:04.611Z

Read this collection of quotes What the Experts Say about Using Variable Annuities for a Guaranteed Income

Read what Capital Group / American Funds says about Variable Annuities (and their "Insurance Series" Sub-Accounts. ARTICLE

Listen to Variable Annuities: When they are useful as a retirement income planning option AUDIO

Presenting VAs¶

Watch VA Napkin Presentation VIDEO

Watch Transition from Mutual Funds to Variable Annuities VIDEO

Watch VA with Guaranteed Income (2023-03) VIDEO

View slides 15 - 16 of Income Planning for Your Golden Years PDF

Generational Wealth Plan¶

Watch Variable Annuity Generational Wealth Napkin Presentation VIDEO

- Build retirement assets in mutual funds, tax-deferred: IRAs, 401ks, "naked" VAs.

- 5 - 7 years from retirement, shelter all retirement accounts (those in step 1) with variable annuities with a guaranteed income rider. Both spouses withdraw their guaranteed income with no concern of worrying about running out of money.

- When both spouses die, the balance of the variable nnuities are inherited by the children, an they start the process (with step 1 above) all over again. Over generations the plan is to keep increasing the overall amount and thus build a legacy income stream.

Venn Diagram of Annuities¶

PHN2ZyB4bWxucz0iaHR0cDovL3d3dy53My5vcmcvMjAwMC9zdmciIHhtbG5zOnhsaW5rPSJodHRwOi8vd3d3LnczLm9yZy8xOTk5L3hsaW5rIiB2ZXJzaW9uPSIxLjEiIHdpZHRoPSI0MjFweCIgaGVpZ2h0PSIzNTBweCIgdmlld0JveD0iLTAuNSAtMC41IDQyMSAzNTAiIGNvbnRlbnQ9IiZsdDtteGZpbGUgaG9zdD0mcXVvdDtlbWJlZC5kaWFncmFtcy5uZXQmcXVvdDsgbW9kaWZpZWQ9JnF1b3Q7MjAyMy0wNC0xOFQyMDo0NDo0NC4wNjlaJnF1b3Q7IGFnZW50PSZxdW90O01vemlsbGEvNS4wIChYMTE7IExpbnV4IHg4Nl82NCkgQXBwbGVXZWJLaXQvNTM3LjM2IChLSFRNTCwgbGlrZSBHZWNrbykgQ2hyb21lLzExMi4wLjAuMCBTYWZhcmkvNTM3LjM2JnF1b3Q7IGV0YWc9JnF1b3Q7YVVIVVdXQ3dOSC1MdTJBSlVJX0gmcXVvdDsgdmVyc2lvbj0mcXVvdDsyMS4xLjkmcXVvdDsgdHlwZT0mcXVvdDtlbWJlZCZxdW90OyZndDsmbHQ7ZGlhZ3JhbSBpZD0mcXVvdDszTG1pYThLTDVicVJVckZsd2JOUiZxdW90OyBuYW1lPSZxdW90O1BhZ2UtMSZxdW90OyZndDszVmpiY3Bzd0VQMGFQMmJHaG1EalIxOXk2eVR0VE5OcG4yVllRRk1oT1VMNGtxL3ZMZ2diWWtpY3hrNW42Z2VEenE1V0srbnNrZXllTzBzM041b3Rrd2NWZ3VnNS9YRFRjK2M5eHhuMHZUNCtDTm1XaURkMlNpRFdQTFJPZStDUlAwUFYwNkk1RHlGck9CcWxoT0hMSmhnb0tTRXdEWXhwcmRaTnQwaUo1cWhMRnNNQjhCZ3djWWorNHFGSlN0U3Zwa1g0TGZBNHFVWWU5SzBsWlpXekJiS0VoV3BkZzl5cm5qdlRTcG55TGQzTVFORGlWZXRTOXJ2dXNPNFMweUROVVIzR1pZOFZFN21kWE04WkN1dzdEZm1LRWpSYk8rdmhVMDVaVFNNbHpVVlc3TWtFSFFhakplN3JkRy9IdDlnK1JlVi9ra0NMRDBVcDlzQkRqNnVubkp0dGp4Ykd4dFVuU1E4WGVkR0NsZE0vZ0l2VmJhTC8yWUkvNUNabnhMWHJYSWJaQ1ZiSmFhVGpJSkd4M3JFeFhTZmN3T09TQldSWm8rUWdscGhVWUd1QXJ5eGJsaUlROFEyRU5BTXV4RXdKcFl0QWJoVEJNQWdRejR4V3Y2Rm1DVWZqQmRMR25jYWFoUnhMcW1hN0xqNDEyNXhySElZcmlYWmdHZVhNQkkrcEdhQVpOSTJBU1hJWjMwTkUrVnhjVXV3VmFNTlJXeWJXMmFqbDN2TUhOZWF1aDRpQmpmbEdxQ0hWOUtpcmFqYkwvQ3RGOHV4ZVdma2NqSGFMV0pjSHF4aVVCR3hxa0pXTEcxQXBHRTNsWXEyT2xlcHRVNUxYZXgxMEtoMU1haHE0QTVuVjNuZ1hlUzlQK0dJVnFsMnRkdGwycU5VQmZVdmdKbWVhNFE3ZzVyL093cTZpN0lpTFQ1YlNac2xGUm84N0dlQ2NpZ09GSk9XZVIvQ2VBYy9GNzlBRFA3eHM0N2Z2TE56aHNJUERheWc0L0JyMWlWN1hMT1dDeUhBTFlnWEU1QmJlZFJYQ2Qwc1E5L0xNaGRBc3ZOR0phbUhnKy8rd0dKeXpIOTBmT3dDcUtMajI4a09CdmlxMFRxVEVjNXMvczRLZSt4SXFveDkxRkovaHpKMEVBV1JaY2YvRUwrUTVrd0djZDBpOFdXb2E4VTRtb0xrNUhQWjA5NW5Qa1NjR2Z0UjYvQTRESHhaUmh6eEpwYW5HM3RBZ20yL2JPYnRReHFqMENJV3JDNW5Wa2FudE8zY0hmeWxJcDFDZlNtNTI2dU45cHZ5NG5mSno5QVhVUDRuK2RFWDV3b0xmR1dsRi8rZmtuYlh4Vm1KSDNXSmZGQXl4NUlEbFVrbG9PeC9yTldKOWFpWDFrc29wRDBQUlZZcGE0ZjJiQ3Erb2dqcWgvZGZLNXhSWHhmNExncnJqQTRJT1cvanB2cCtlMk56L2FDNXN0YjhlM0tzLyZsdDsvZGlhZ3JhbSZndDsmbHQ7L214ZmlsZSZndDsiPjxkZWZzPjxsaW5lYXJHcmFkaWVudCB4MT0iMCUiIHkxPSIwJSIgeDI9IjEwMCUiIHkyPSIwJSIgaWQ9Im14LWdyYWRpZW50LWZmZTZjYy0xLWZmZmZmZi0xLWUtMCI+PHN0b3Agb2Zmc2V0PSIwJSIgc3R5bGU9InN0b3AtY29sb3I6IHJnYigyNTUsIDIzMCwgMjA0KTsgc3RvcC1vcGFjaXR5OiAxOyIvPjxzdG9wIG9mZnNldD0iMTAwJSIgc3R5bGU9InN0b3AtY29sb3I6IHJnYigyNTUsIDI1NSwgMjU1KTsgc3RvcC1vcGFjaXR5OiAxOyIvPjwvbGluZWFyR3JhZGllbnQ+PGxpbmVhckdyYWRpZW50IHgxPSIxMDAlIiB5MT0iMCUiIHgyPSIwJSIgeTI9IjAlIiBpZD0ibXgtZ3JhZGllbnQtZmZmZmZmLTEtZDVlOGQ0LTEtZS0wIj48c3RvcCBvZmZzZXQ9IjAlIiBzdHlsZT0ic3RvcC1jb2xvcjogcmdiKDIxMywgMjMyLCAyMTIpOyBzdG9wLW9wYWNpdHk6IDE7Ii8+PHN0b3Agb2Zmc2V0PSIxMDAlIiBzdHlsZT0ic3RvcC1jb2xvcjogcmdiKDI1NSwgMjU1LCAyNTUpOyBzdG9wLW9wYWNpdHk6IDE7Ii8+PC9saW5lYXJHcmFkaWVudD48bGluZWFyR3JhZGllbnQgeDE9IjAlIiB5MT0iMTAwJSIgeDI9IjAlIiB5Mj0iMCUiIGlkPSJteC1ncmFkaWVudC1mZmZmZmYtMS1kYWU4ZmMtMS1zLTAiPjxzdG9wIG9mZnNldD0iMCUiIHN0eWxlPSJzdG9wLWNvbG9yOiByZ2IoMjE4LCAyMzIsIDI1Mik7IHN0b3Atb3BhY2l0eTogMTsiLz48c3RvcCBvZmZzZXQ9IjEwMCUiIHN0eWxlPSJzdG9wLWNvbG9yOiByZ2IoMjU1LCAyNTUsIDI1NSk7IHN0b3Atb3BhY2l0eTogMTsiLz48L2xpbmVhckdyYWRpZW50PjwvZGVmcz48Zz48ZWxsaXBzZSBjeD0iMTI3IiBjeT0iMTI3IiByeD0iMTI1IiByeT0iMTI1IiBmaWxsLW9wYWNpdHk9IjAuNSIgZmlsbD0idXJsKCNteC1ncmFkaWVudC1mZmU2Y2MtMS1mZmZmZmYtMS1lLTApIiBzdHJva2U9IiNkNzliMDAiIHN0cm9rZS1vcGFjaXR5PSIwLjUiIHN0cm9rZS13aWR0aD0iNSIgcG9pbnRlci1ldmVudHM9ImFsbCIvPjxnIHRyYW5zZm9ybT0idHJhbnNsYXRlKC0wLjUgLTAuNSkiIG9wYWNpdHk9IjAuNSI+PHN3aXRjaD48Zm9yZWlnbk9iamVjdCBwb2ludGVyLWV2ZW50cz0ibm9uZSIgd2lkdGg9IjEwMCUiIGhlaWdodD0iMTAwJSIgcmVxdWlyZWRGZWF0dXJlcz0iaHR0cDovL3d3dy53My5vcmcvVFIvU1ZHMTEvZmVhdHVyZSNFeHRlbnNpYmlsaXR5IiBzdHlsZT0ib3ZlcmZsb3c6IHZpc2libGU7IHRleHQtYWxpZ246IGxlZnQ7Ij48ZGl2IHhtbG5zPSJodHRwOi8vd3d3LnczLm9yZy8xOTk5L3hodG1sIiBzdHlsZT0iZGlzcGxheTogZmxleDsgYWxpZ24taXRlbXM6IHVuc2FmZSBmbGV4LXN0YXJ0OyBqdXN0aWZ5LWNvbnRlbnQ6IHVuc2FmZSBjZW50ZXI7IHdpZHRoOiAyODhweDsgaGVpZ2h0OiAxcHg7IHBhZGRpbmctdG9wOiA0NHB4OyBtYXJnaW4tbGVmdDogLTM3cHg7Ij48ZGl2IGRhdGEtZHJhd2lvLWNvbG9ycz0iY29sb3I6IHJnYigwLCAwLCAwKTsgIiBzdHlsZT0iYm94LXNpemluZzogYm9yZGVyLWJveDsgZm9udC1zaXplOiAwcHg7IHRleHQtYWxpZ246IGNlbnRlcjsiPjxkaXYgc3R5bGU9ImRpc3BsYXk6IGlubGluZS1ibG9jazsgZm9udC1zaXplOiAxN3B4OyBmb250LWZhbWlseTogSGVsdmV0aWNhOyBjb2xvcjogcmdiKDAsIDAsIDApOyBsaW5lLWhlaWdodDogMS4yOyBwb2ludGVyLWV2ZW50czogYWxsOyB3aGl0ZS1zcGFjZTogbm9ybWFsOyBvdmVyZmxvdy13cmFwOiBub3JtYWw7Ij48ZGl2IHN0eWxlPSJmb250LXNpemU6IDE3cHg7Ij48Zm9udCBzdHlsZT0iZm9udC1zaXplOiAxN3B4OyI+PGIgc3R5bGU9ImZvbnQtc2l6ZTogMTdweDsiPjEwMCUgRXF1aXR5IDxiciBzdHlsZT0iZm9udC1zaXplOiAxN3B4OyIgLz48L2I+PC9mb250PjwvZGl2PjxkaXYgc3R5bGU9ImZvbnQtc2l6ZTogMTdweDsiPjxmb250IHN0eWxlPSJmb250LXNpemU6IDE3cHg7Ij48YiBzdHlsZT0iZm9udC1zaXplOiAxN3B4OyI+TXV0dWFsIEZ1bmRzPC9iPjwvZm9udD48L2Rpdj48L2Rpdj48L2Rpdj48L2Rpdj48L2ZvcmVpZ25PYmplY3Q+PHRleHQgeD0iMTA3IiB5PSI2MSIgZmlsbD0icmdiKDAsIDAsIDApIiBmb250LWZhbWlseT0iSGVsdmV0aWNhIiBmb250LXNpemU9IjE3cHgiIHRleHQtYW5jaG9yPSJtaWRkbGUiPjEwMCUgRXF1aXR5Li4uPC90ZXh0Pjwvc3dpdGNoPjwvZz48ZWxsaXBzZSBjeD0iMjkzIiBjeT0iMTI3IiByeD0iMTI1IiByeT0iMTI1IiBmaWxsLW9wYWNpdHk9IjAuNSIgZmlsbD0idXJsKCNteC1ncmFkaWVudC1mZmZmZmYtMS1kNWU4ZDQtMS1lLTApIiBzdHJva2U9IiM4MmIzNjYiIHN0cm9rZS1vcGFjaXR5PSIwLjUiIHN0cm9rZS13aWR0aD0iNSIgcG9pbnRlci1ldmVudHM9ImFsbCIvPjxnIHRyYW5zZm9ybT0idHJhbnNsYXRlKC0wLjUgLTAuNSkiIG9wYWNpdHk9IjAuNSI+PHN3aXRjaD48Zm9yZWlnbk9iamVjdCBwb2ludGVyLWV2ZW50cz0ibm9uZSIgd2lkdGg9IjEwMCUiIGhlaWdodD0iMTAwJSIgcmVxdWlyZWRGZWF0dXJlcz0iaHR0cDovL3d3dy53My5vcmcvVFIvU1ZHMTEvZmVhdHVyZSNFeHRlbnNpYmlsaXR5IiBzdHlsZT0ib3ZlcmZsb3c6IHZpc2libGU7IHRleHQtYWxpZ246IGxlZnQ7Ij48ZGl2IHhtbG5zPSJodHRwOi8vd3d3LnczLm9yZy8xOTk5L3hodG1sIiBzdHlsZT0iZGlzcGxheTogZmxleDsgYWxpZ24taXRlbXM6IHVuc2FmZSBmbGV4LXN0YXJ0OyBqdXN0aWZ5LWNvbnRlbnQ6IHVuc2FmZSBjZW50ZXI7IHdpZHRoOiAxMzdweDsgaGVpZ2h0OiAxcHg7IHBhZGRpbmctdG9wOiA0NHB4OyBtYXJnaW4tbGVmdDogMjQ2cHg7Ij48ZGl2IGRhdGEtZHJhd2lvLWNvbG9ycz0iY29sb3I6IHJnYigwLCAwLCAwKTsgIiBzdHlsZT0iYm94LXNpemluZzogYm9yZGVyLWJveDsgZm9udC1zaXplOiAwcHg7IHRleHQtYWxpZ246IGNlbnRlcjsiPjxkaXYgc3R5bGU9ImRpc3BsYXk6IGlubGluZS1ibG9jazsgZm9udC1zaXplOiAxN3B4OyBmb250LWZhbWlseTogSGVsdmV0aWNhOyBjb2xvcjogcmdiKDAsIDAsIDApOyBsaW5lLWhlaWdodDogMS4yOyBwb2ludGVyLWV2ZW50czogYWxsOyB3aGl0ZS1zcGFjZTogbm9ybWFsOyBvdmVyZmxvdy13cmFwOiBub3JtYWw7Ij48ZGl2PjxiPkd1YXJhbnRlZWQ8L2I+PC9kaXY+PGRpdj48Yj7CoEluY29tZSBmb3IgTGlmZTwvYj48L2Rpdj48L2Rpdj48L2Rpdj48L2Rpdj48L2ZvcmVpZ25PYmplY3Q+PHRleHQgeD0iMzE1IiB5PSI2MSIgZmlsbD0icmdiKDAsIDAsIDApIiBmb250LWZhbWlseT0iSGVsdmV0aWNhIiBmb250LXNpemU9IjE3cHgiIHRleHQtYW5jaG9yPSJtaWRkbGUiPkd1YXJhbnRlZWQuLi48L3RleHQ+PC9zd2l0Y2g+PC9nPjxlbGxpcHNlIGN4PSIyMTUiIGN5PSIyMjIiIHJ4PSIxMjUiIHJ5PSIxMjUiIGZpbGwtb3BhY2l0eT0iMC41IiBmaWxsPSJ1cmwoI214LWdyYWRpZW50LWZmZmZmZi0xLWRhZThmYy0xLXMtMCkiIHN0cm9rZT0iIzZjOGViZiIgc3Ryb2tlLW9wYWNpdHk9IjAuNSIgc3Ryb2tlLXdpZHRoPSI1IiBwb2ludGVyLWV2ZW50cz0iYWxsIi8+PGcgdHJhbnNmb3JtPSJ0cmFuc2xhdGUoLTAuNSAtMC41KSIgb3BhY2l0eT0iMC41Ij48c3dpdGNoPjxmb3JlaWduT2JqZWN0IHBvaW50ZXItZXZlbnRzPSJub25lIiB3aWR0aD0iMTAwJSIgaGVpZ2h0PSIxMDAlIiByZXF1aXJlZEZlYXR1cmVzPSJodHRwOi8vd3d3LnczLm9yZy9UUi9TVkcxMS9mZWF0dXJlI0V4dGVuc2liaWxpdHkiIHN0eWxlPSJvdmVyZmxvdzogdmlzaWJsZTsgdGV4dC1hbGlnbjogbGVmdDsiPjxkaXYgeG1sbnM9Imh0dHA6Ly93d3cudzMub3JnLzE5OTkveGh0bWwiIHN0eWxlPSJkaXNwbGF5OiBmbGV4OyBhbGlnbi1pdGVtczogdW5zYWZlIGZsZXgtZW5kOyBqdXN0aWZ5LWNvbnRlbnQ6IHVuc2FmZSBjZW50ZXI7IHdpZHRoOiAyNDhweDsgaGVpZ2h0OiAxcHg7IHBhZGRpbmctdG9wOiAzMTNweDsgbWFyZ2luLWxlZnQ6IDkxcHg7Ij48ZGl2IGRhdGEtZHJhd2lvLWNvbG9ycz0iY29sb3I6IHJnYigwLCAwLCAwKTsgIiBzdHlsZT0iYm94LXNpemluZzogYm9yZGVyLWJveDsgZm9udC1zaXplOiAwcHg7IHRleHQtYWxpZ246IGNlbnRlcjsiPjxkaXYgc3R5bGU9ImRpc3BsYXk6IGlubGluZS1ibG9jazsgZm9udC1zaXplOiAxN3B4OyBmb250LWZhbWlseTogSGVsdmV0aWNhOyBjb2xvcjogcmdiKDAsIDAsIDApOyBsaW5lLWhlaWdodDogMS4yOyBwb2ludGVyLWV2ZW50czogYWxsOyB3aGl0ZS1zcGFjZTogbm9ybWFsOyBvdmVyZmxvdy13cmFwOiBub3JtYWw7Ij48ZGl2IHN0eWxlPSJmb250LXNpemU6IDE3cHg7Ij48YiBzdHlsZT0iZm9udC1zaXplOiAxN3B4OyI+PHNwYW4gc3R5bGU9ImZvbnQtc2l6ZTogMTdweDsiPk5vIEFubnVpdGl6YXRpb248L3NwYW4+PC9iPjwvZGl2PjxkaXYgc3R5bGU9ImZvbnQtc2l6ZTogMTdweDsiPkFjY2VzcyB0byBCYWxhbmNlPC9kaXY+PGRpdiBzdHlsZT0iZm9udC1zaXplOiAxN3B4OyI+SGVpcnMgSW5oZXJpdCBCYWxhbmNlPGJyIHN0eWxlPSJmb250LXNpemU6IDE3cHg7IiAvPjwvZGl2PjwvZGl2PjwvZGl2PjwvZGl2PjwvZm9yZWlnbk9iamVjdD48dGV4dCB4PSIyMTUiIHk9IjMxMyIgZmlsbD0icmdiKDAsIDAsIDApIiBmb250LWZhbWlseT0iSGVsdmV0aWNhIiBmb250LXNpemU9IjE3cHgiIHRleHQtYW5jaG9yPSJtaWRkbGUiPk5vIEFubnVpdGl6YXRpb24uLi48L3RleHQ+PC9zd2l0Y2g+PC9nPjxyZWN0IHg9IjE4MCIgeT0iMTMxIiB3aWR0aD0iNjAiIGhlaWdodD0iMzAiIGZpbGw9Im5vbmUiIHN0cm9rZT0ibm9uZSIgcG9pbnRlci1ldmVudHM9ImFsbCIvPjxnIHRyYW5zZm9ybT0idHJhbnNsYXRlKC0wLjUgLTAuNSkiPjxzd2l0Y2g+PGZvcmVpZ25PYmplY3QgcG9pbnRlci1ldmVudHM9Im5vbmUiIHdpZHRoPSIxMDAlIiBoZWlnaHQ9IjEwMCUiIHJlcXVpcmVkRmVhdHVyZXM9Imh0dHA6Ly93d3cudzMub3JnL1RSL1NWRzExL2ZlYXR1cmUjRXh0ZW5zaWJpbGl0eSIgc3R5bGU9Im92ZXJmbG93OiB2aXNpYmxlOyB0ZXh0LWFsaWduOiBsZWZ0OyI+PGRpdiB4bWxucz0iaHR0cDovL3d3dy53My5vcmcvMTk5OS94aHRtbCIgc3R5bGU9ImRpc3BsYXk6IGZsZXg7IGFsaWduLWl0ZW1zOiB1bnNhZmUgY2VudGVyOyBqdXN0aWZ5LWNvbnRlbnQ6IHVuc2FmZSBjZW50ZXI7IHdpZHRoOiA1OHB4OyBoZWlnaHQ6IDFweDsgcGFkZGluZy10b3A6IDE0NnB4OyBtYXJnaW4tbGVmdDogMTgxcHg7Ij48ZGl2IGRhdGEtZHJhd2lvLWNvbG9ycz0iY29sb3I6IHJnYigwLCAwLCAwKTsgIiBzdHlsZT0iYm94LXNpemluZzogYm9yZGVyLWJveDsgZm9udC1zaXplOiAwcHg7IHRleHQtYWxpZ246IGNlbnRlcjsiPjxkaXYgc3R5bGU9ImRpc3BsYXk6IGlubGluZS1ibG9jazsgZm9udC1zaXplOiAxOHB4OyBmb250LWZhbWlseTogSGVsdmV0aWNhOyBjb2xvcjogcmdiKDAsIDAsIDApOyBsaW5lLWhlaWdodDogMS4yOyBwb2ludGVyLWV2ZW50czogYWxsOyB3aGl0ZS1zcGFjZTogbm9ybWFsOyBvdmVyZmxvdy13cmFwOiBub3JtYWw7Ij48Zm9udCBzdHlsZT0iZm9udC1zaXplOiAxOHB4OyI+PGIgc3R5bGU9ImZvbnQtc2l6ZTogMThweDsiPkphY2tzb24gVkE8YnIgc3R5bGU9ImZvbnQtc2l6ZTogMThweDsiIC8+PC9iPjwvZm9udD48L2Rpdj48L2Rpdj48L2Rpdj48L2ZvcmVpZ25PYmplY3Q+PHRleHQgeD0iMjEwIiB5PSIxNTEiIGZpbGw9InJnYigwLCAwLCAwKSIgZm9udC1mYW1pbHk9IkhlbHZldGljYSIgZm9udC1zaXplPSIxOHB4IiB0ZXh0LWFuY2hvcj0ibWlkZGxlIj5KYWNrc29uLi4uPC90ZXh0Pjwvc3dpdGNoPjwvZz48L2c+PHN3aXRjaD48ZyByZXF1aXJlZEZlYXR1cmVzPSJodHRwOi8vd3d3LnczLm9yZy9UUi9TVkcxMS9mZWF0dXJlI0V4dGVuc2liaWxpdHkiLz48YSB0cmFuc2Zvcm09InRyYW5zbGF0ZSgwLC01KSIgeGxpbms6aHJlZj0iaHR0cHM6Ly93d3cuZGlhZ3JhbXMubmV0L2RvYy9mYXEvc3ZnLWV4cG9ydC10ZXh0LXByb2JsZW1zIiB0YXJnZXQ9Il9ibGFuayI+PHRleHQgdGV4dC1hbmNob3I9Im1pZGRsZSIgZm9udC1zaXplPSIxMHB4IiB4PSI1MCUiIHk9IjEwMCUiPlRleHQgaXMgbm90IFNWRyAtIGNhbm5vdCBkaXNwbGF5PC90ZXh0PjwvYT48L3N3aXRjaD48L3N2Zz4=

Currently, the only VA I know of that meet the cross-section of the 3 points above is Jackson.

Understanding VAs¶

“In practice, the word 'annuity' is a broad and consequently almost meaningless term.” -Moshe Milevsky

"Variable Annuities allow you to invest in the world's great companies, while simultaneously guaranteeing that your retirement income will never go down (but probably go up).

Lesson: Social Security income + VA income should cover one’s bills and basic needs during retirement. The rest should be in 100% equity mutual funds." -Michael Thomas

Read Nick's On Panic, Faith, and the Determined Primitive PDF

Read John Huggard's HOW TO NEGATE THE TEN MOST COMMON UNFOUNDED OBJECTIONS TO VARIABLE ANNUITY OWNERSHIP PDF

Read John Huggard's Understanding New VA Riders PDF

Read Why put an IRA in anything but a VA PDF

Read Funding Trusts & Annuities PDF

Watch Variable Annuities Overview VIDEO

Watch Annuities for a Biological Age by Moshe Milvesky VIDEO

Watch Client Case Study: 10-Year Reset of Income Rider Step-Up VIDEO

Investing with Variable Annuities by John P. Huggard BOOK Dispels the many myths about variable annuities and provides valuable tax data.

Just as life insurance offers protection against dying too soon, an annuity offers protection against living too long; in other words, outliving one's income.

-

The mutual fund company is the money manager, and the variable annuity is the risk manager.

-

Modern VAs are all B-shares which means there is no upfront sales charge (all of your client's money is 100% investest immediately), but they do have a surrender charge that usually lasts 7 years.

-

Tax-Deferred Compounding. All earnings accumulate tax-deferred until withdrawn. A variable annuity also offers a means of accumulating money on a tax deferred basis. If you have already maximized your contributions to an IRA or company savings plan, or if you've received a lump sum resulting from an inheritance or other settlement, you may want to consider saving in a variable annuity.

-

The long-term goal of investing is to multiply the eggs in our basket. Most people are very focused on producing more eggs (getting high returns) but pay little attention to the fox that perpetually robs the hen house. If you ignore the fox, soon there will be nothing left to produce more eggs. That fox is taxation. Annuities build a high fence around the hen house and keeps the foxes out, allowing your eggs to multiply.

A study done by PricewaterhouseCoopers concluded that variable annuities, even with a slightly-higher fee structure, are a very attractive investment compared to mutual funds for long-term savers. The study compared the after-tax returns from mutual funds and variable annuities to calculate the “break-even holding period.” For accumulations longer than the break-even period, after-tax payouts from variable annuity investments exceed those from comparable mutual fund investments. According to the study, the benefits of tax-deferral make up for higher costs within 5.1 years.

-QuestCE study program Suitability of Variable Annuity Products (2024)

-

Multiple subaccount choices in one product. A variable annuity is one that has mutual funds inside of it, called "sub-accounts". Usually they offer a very broad selection of investment options from a variety of leading fund managers. When you purchase a variable annuity, you allocate your money to the fund or funds of your choice, depending on your investment and risk profile at that time. Contract owner can re-allocate cash values without tax consequences.

-

Rebalancing. Over time, money allocated to different funding options will grow at different rates. This means that the allocation of your assets may become "out of alignment" with the strategy that you chose. Additionally, throughout your life cycle, your objectives and risk tolerance may change. Within the annuity, you can change the funds to which your money is allocated at any time, without charge or any income tax consequences. You also have the option to enroll, without charge, in an Automatic Portfolio Rebalancing Program which automatically restores your allocation to a desired percentage on a periodic basis.

-

Unlimited Contributions. No cap on amount invested in a non-qualified annuity.

-

Guaranteed death benefit. The "standard" death benefit guarantees that if you die your heirs will receive the greater of the original purchase payment or the contract value at death (minus your withdrawals). Most annuities also offer a "stepped-up benefit" that locks in investment gains every year. This gives you the confidence to invest in the stock market, which is important in order to keep pace with inflation, and to know that your family will be protected against financial loss in the event of an untimely death.

-

No (or limited) probate.

-

Flexible investment strategies.

-

Dollar Cost Averaging. You can set up an automatic monthly transfer from your checking account into your VA.

-

Guaranteed Lifetime Income. Only investment that can provide guaranteed lifetime income, with an income-rider (see below).

Selecting the Sub-Accounts (mutual funds)¶

“Allocating 100% to stocks is perfectly rational and economically suitable within the variable annuity.” -Moshe Milevsky, Section II from the book In Defense of Annuities.

- This is the most important step. Remember, investing in the market is "Plan A". The Income Rider is "Plan B".

Jackson Sub-Accounts¶

For long-term growth and/or with an income rider I recommend:

- 25%: JNL/American Funds Growth (395)

- 25%: JNL/American Funds Growth-Income (342)

- 20%: JNL/American Funds Global Growth (638)

- 15%: JNL/Mellon Nasdaq 100 Index (222)

- 15%: JNL/Mellon Information Technology Sector (187)

Guaranteed Income Rider¶

Watch Simply Explaining VA Income Riders VIDEO

"I know of only two ways of coping with equity volatility during retirement withdrawals:

Abiding faith in the historical record, in the greatness of free-market democratic capitalism.

The other method is what the variable annuity industry is pleased to call “living benefits.”

-Nick Murray, On Panic, Faith, and the Determined Primitive

"Insurance companies promise that annuitants won't run out of income, ever! When there is a living benefit, an annuitant may run out of cash but not out of income.” -Richard Hoe, ChFC, CLU, AEP. From the article "The Better IRA" in The Investment Edge magazine.

When marketing variable annuities with guaranteed income riders, please keep "Plan A" as the primary focus.

- Plan A = equity mutual funds, the drivers of the account growth. The engine.

- Plan B = the guarantees of the income rider that protect the income if the client withdraws in a down market. The airbag.

There are cases where the features of the GIR supersede the mutual funds selections within the variable annuity. However, don't get caught in a "rider war" and find yourself selling a VA just on the GIR features. Keep the main thing, the main thing - investing in the Great Companies of the World.

“Win-Win Situation: - If the market goes up - you're a winner. - If the market goes down - you're a winner. - No more disgruntled clients.

-John Huggard, Page 42 from his lecture notes, "Understanding the New Variable Annuity Living Benefit Riders" (January 8, 2007).

The simplest way to describe this product, using the Jackson VA as an example, is...

With this product, called a variable annuity with guaranteed income, we're building a "private pension" or "personal social security". Compare it to social security, but with improvements:

-

Your income starts at age 65 and is at least 5% of your account value at that time (up to 8.3% but never less than 5%).

-

Your first income check is your smallest check - ever. Meaning, when you account value goes up, your income goes up (and that becomes the new minimum). When you account goes down, your income stays the same.

-

If one spouse dies, the other spouse continues getting the income until he/she passes. (And keeps getting the income from his/her own annuity, of course).

-

When both spouses passes, the balance of the account goes to the children.

-

If at anytime you want your account balance, you can close the account and take the cash.

There is more to it than the above, such as the guaranteed 6% growth before taking withdrawals, but I don't want to over complicate it.

Other Benefits¶

1035 Exchange¶

Watch AF MKOM 1673 - Variable Annuity 1035 Exchanges VIDEO

Watch 1035 Exchanges from Cash-Value Life Policies 1 VIDEO

Watch 1035 Exchanges from Cash-Value Life Policies 2 VIDEO

Section 1035 of the Internal Revenue Code allows you to do a tax-free exchange from a life insurance policy or annuity to an annuity. Article: Just say no to no cash values.

Reasons you may want to move from VA to VA¶

- Rolling over from old VAs where the cash is more than the income base, will reset the NEW income to a higher level. You can do the same thing for the death benefit.

- A lot of old VAs were "single-life" only, and clients are moving to new VA to get the Joint-life.

- For non-qualified money the tax savings on i4Life.

- Lower fees.

- Better sub-accounts.

- Better income riders.

- Better death benefit.

Carrying Over a GAIN from Cash-Value Life Insurance Policy¶

If you have a gain in your life insurance policy (ie, the surrender value of the policy is more than the total premiums), a 1035-exchange lets you defer paying income tax on those gains until you begin withdrawals from your annuity, instead of paying them now when you close your policy..

Cash-Value Policy

- $10,000 in premiums (cost basis)

- $12,000 surrender value

- $2,000 gain

If you surrender your policy now, then you immediately pay taxes on the $2,000 gain. Instead, do a 1035-Exchange to a Variable Annuity:

- $12,000 gets rolled over and deposited in the VA.

- The $10,000 cost-basis gets carried over.

Only $2,000 is considered "profit" (not the entire $12,000) and is taxable upon withdrawal (not before).

Carrying Over a LOSS from a Cash-Value Life Insurance Policy¶

This is specific to transferring the cash-value of a life insurance policy to a variable annuity using the 1035-Exchange.

"But it is easy to suffer losses with "cash value’ life, which combines a death benefit with a savings or investment account. ... If the policy's cash value—also called the "surrender value"—is lower than the total premiums you paid in, too bad: You can't deduct the loss or use it to offset gains in other investments."

-Conquering Retirement: How Insurance Can Cut Your Taxes, Wall Street Journal, Nov 30, 2012

If you have a loss in your life insurance policy (ie, the surrender value of the policy is less than the total premiums), then you cannot deduct those losses. But with a 1035-exchange the loss carries over to the annuity, and it can then be used to avoid paying income tax on future gains up to the cost-basis. This is also called "Preserving a Loss".

Cash-Value Policy

- $10,000 in premiums (cost basis)

- $6,000 surrender value

- $4,000 loss

Variable Annuity

- $6,000 gets rolled over and deposited in the VA.

- The $10,000 cost-basis gets carried over.

You only pay taxes on anything over $10,000 (upon withdrawal).

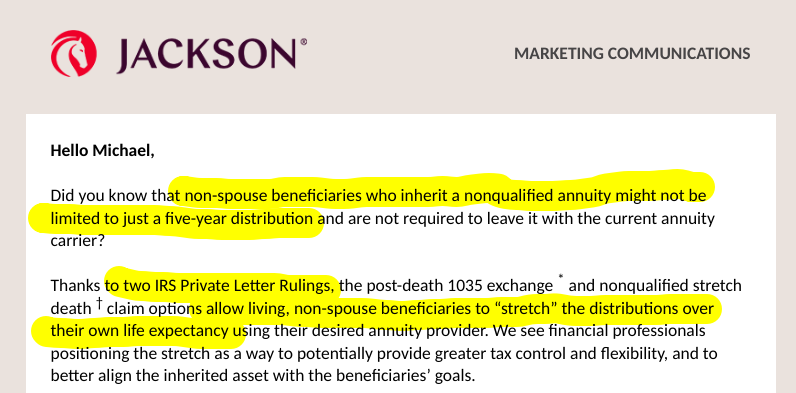

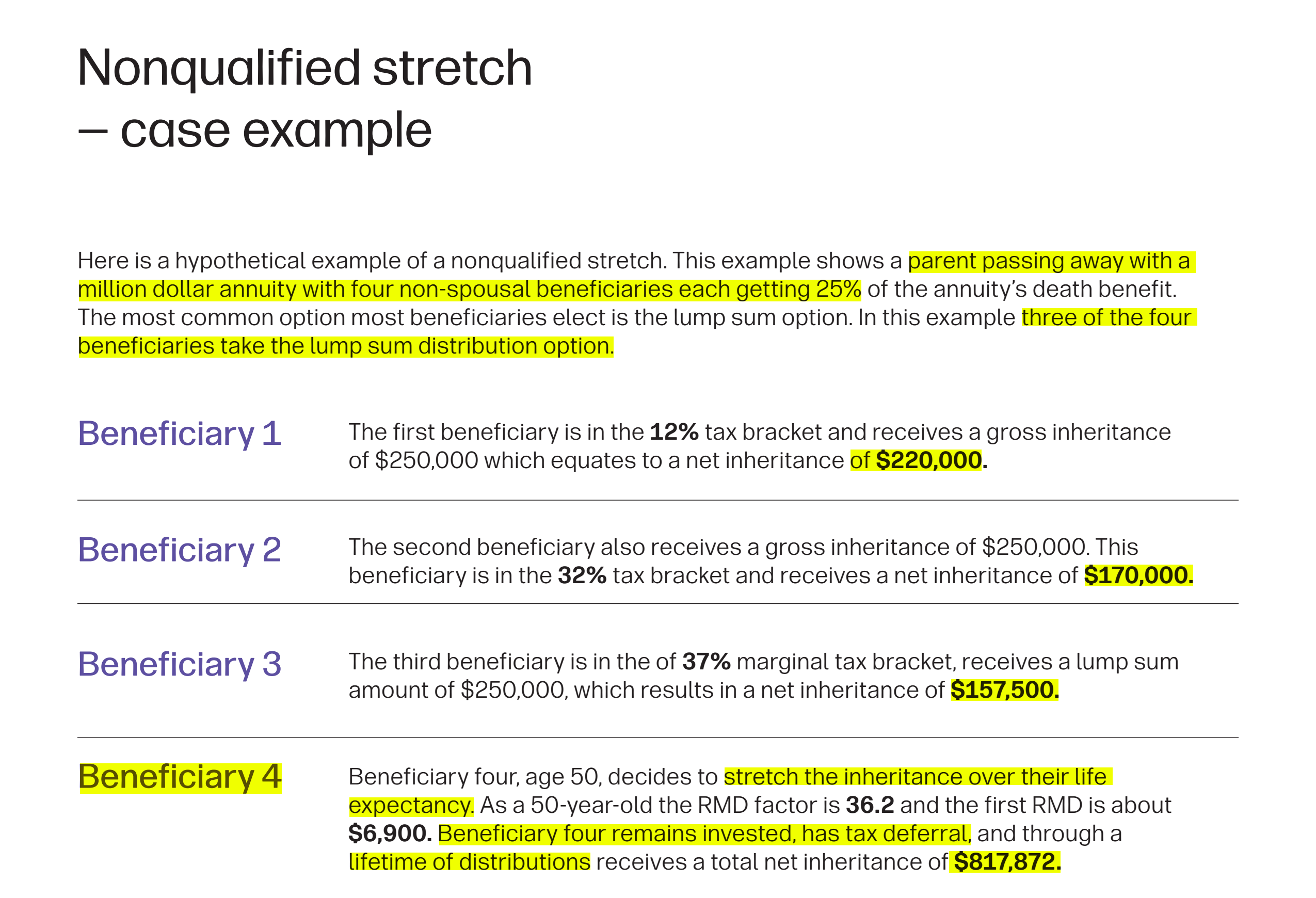

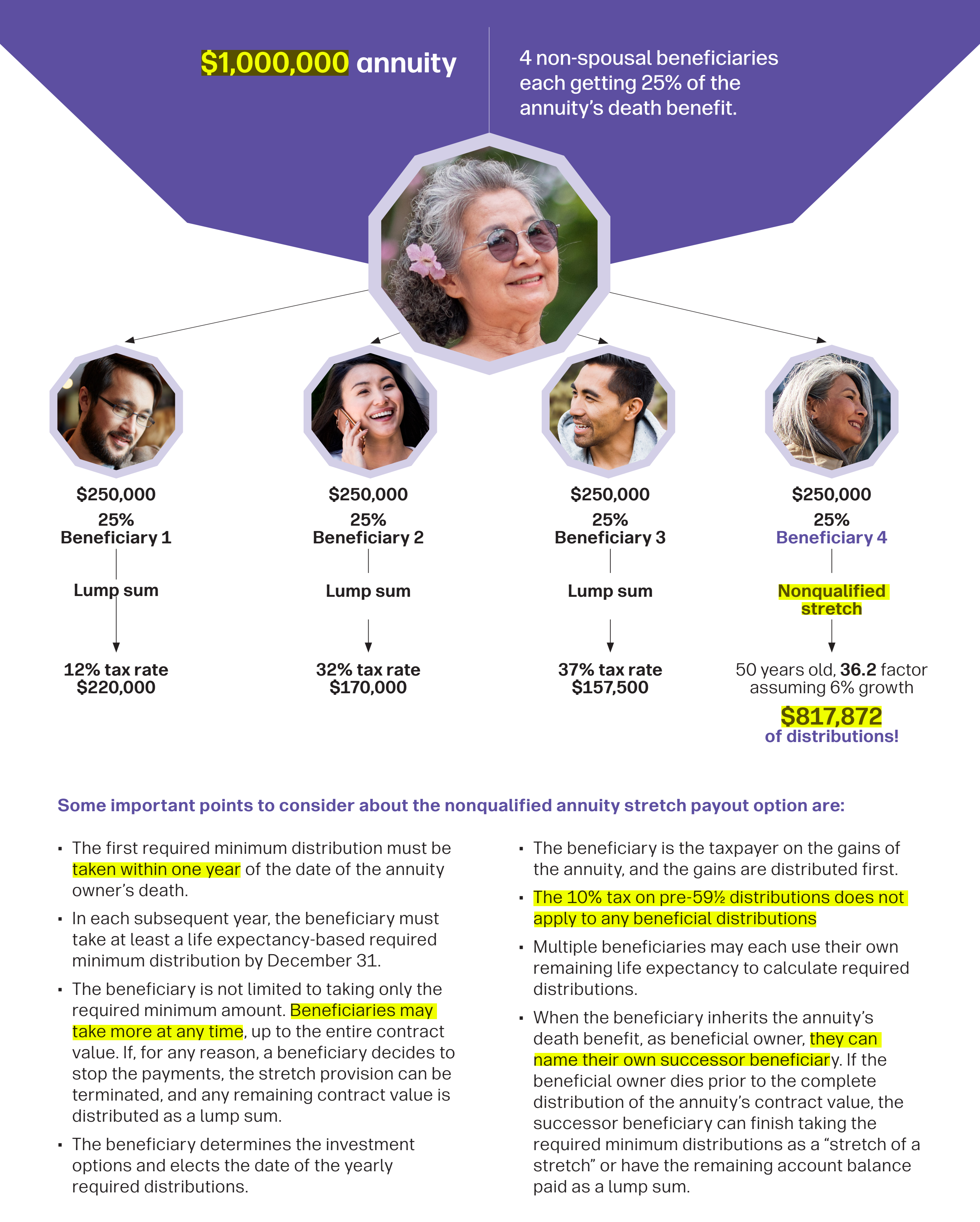

Non-Qualifed Stretch¶

Watch AF MKOM 1672 - VA 1035 & Beni Stretch VIDEO

Read this 3-pages brochure for details and a great example.

VA Gurus¶

John Huggard¶

John Huggard, J.D., CFP, CLU, ChFC, is a sought after expert witness in securities cases and a nationally recognized speaker on the topic of variable annuities.

He received his undergraduate degree and law degree from the University of North Carolina at Chapel Hill and his master’s degree from Duke University. He is now a retired university professor who taught law and finance courses at North Carolina State University for thirty-two years. He was a member of the University’s Academy of Outstanding Teachers and was named an Alumni Distinguished Professor in 1994.

He continues to write and do research at the University on topics that deal with variable annuities. John is currently the senior member of a Raleigh, North Carolina law firm that was founded in 1975. He is a board certified specialist in estate planning and probate law and limits his practice to consultation in the areas of estate planning and financial litigation.

John is the author of several financial magazine articles and books. His two most recent books discuss investing with variable annuities and debunking the myths surrounding variable annuities.

Quotes by John Huggard¶

“Living Benefits are not new variable annuities but riders available with existing variable annuities. Often, only a box on the application nee be checked to obtain a specific living Benefit. Living benefit riders provide long-term investors with: - An opportunity to obtain stock market gaines if the market goes up. - An opportunity to obtain an upward ratcheting lifetime stream of income regardless of the stock market's future direction without annuitization. - The ability to avoid the 'longevity problem' for both spouses. - The ability to avoid the 'sequence of return' trap. - The advantages of obtaining basic variable annuity benefits (commission-free investing, no transaction cots, death benefit, etc.).”

-John Huggard, page 8 from his lecture notes, "Understanding the New Variable Annuity Living Benefit Riders" (January 8, 2007).

Books by John Huggard¶

Moshe A. Milevsky¶

Moshe Arye Milesky is a tenured professor at York University. He has a Ph.D. in Finance, a Master of Arts in Mathematics and cum laude from Yeshiva University. He is a lifetime Fellow of the Fields Institute for Research in Mathematical Sciences. Over the last 25 years he has published 15 books and 60 peer-reviewed scholarly articles on wealth and risk management. He currently serves as a member of the editorial boards for the Journal of Pension Economics and Finance (JPEF), and Insurance: Mathematics and Economics (IME).

Quotes by Moshe Milevsky¶

“I purchased a variable annuity with a guaranteed living benefit and allocated 100% to stocks.” -Moshe Milevsky, End Notes from the book In Defense of Annuities (2021).

“... with a guaranteed and predictable lifetime of income that can't be outlived” -Moshe Milevsky, Section IV from the book In Defense of Annuities (2021).

“A living benefit is paid to the annuitant for as long as they live and ceases upon death.” -Moshe Milevsky, Section V from the book In Defense of Annuities (2021).

“It protects against the risk of living beyond, even far beyond, life expectancy - without surrendering either upside potential of liquidity of the underlying portfolio.” -Moshe Milevsky, Section V from the book In Defense of Annuities (2021).

“The income is guaranteed to never decline for the remaining life of the annuitant. If the underlying investment portfolio ever reaches zero, the guaranteed income will continue so long as the annuitant or, for a joint product, one member of the couple is still alive. Whatever remains in the account at the time of death goes to the heirs.” -Moshe Milevsky, Section V from the book In Defense of Annuities (2021).

“Fees and periodic withdrawals are deducted from the VA account as long as there are funds available. But if those periodic withdrawals every fully deplete this account, the insurance component is triggered to fulfill the remaining withdrawals for the lifetime of the investor.” -Moshe Milevsky, Section V from the book In Defense of Annuities (2021).

“... to provide an assortment of lifetime income guarantees meant to protect the policyholder against longevity risk as well as what the industry has coined as ‘sequence-of-returns risk’, which refers to the chance that a retirement portfolio, from which cash is being withdrawn, suffers early losses, magnified by the retiree living longer than average. All you need is a bear market at the wrong time, and the sustainability of your income can be cut dramatically.” -Moshe Milevsky, Section V from the book In Defense of Annuities (2021).

“By promising a lifetime of retirement income, insurance companies are taking on the above-noted longevity risk.” -Moshe Milevsky, Section V from the book In Defense of Annuities (2021).

“Invest aggressively, diversify, exposure to equities, and wrap some protection around it. Optimize your variable annuity by having an aggressive allocation and protecting it with a lifetime income.” -Moshe Milevsky, from his Annuities for a Biological Age webinar (2020).

Videos by Moshe Milevsky¶

Watch Annuities for a Biological Age. Moshe gives a presentation on a Jackson webinar October 2020 VIDEO

Books by Moshe Milevsky¶

In Defense of Annuities (2021) by Moshe Milevsky BOOK n this brief monograph the author lays-out the financial economic “case” for using annuities while building wealth prior to retirement, as well as for those spending their nest egg in retirement.