IAR vs RR¶

A investment advisor representative (IAR) is someone who has completed the qualifications to be registered with the SEC and with applicable state agencies. A IAR charges based on the percentage of assets that are under management. A IAR is required by law to act as a fiduciary to clients. This means that the client’s benefit is the most important thing to be considered when making recommendations. IARs are required to meet certain standards, and this is enforced by law.

A registered representative (RR) of a broker dealer is someone who facilitates investment transactions. A RR receives his or her compensation through commissions. These commissions are based on investment transactions made on your behalf. However, you have to be aware that a RR isn’t required to meet fiduciary standard, but the SEC does require the RR to make “suitable” recommendations, as well as let you know if there are any conflicts of interest.

Innovation Partners Advisory Platform¶

The IP Advisory Fee-Based Platform opens up a whole new world of opportunity for your business. Many higher net worth clients desire and require active management of their account. Our platform allows the advisor to provide that extra level of service building and managing the account and be compensated more than other types of investments connected with smaller mutual fund accounts.

Many advisors start out with the “bread and butter” client accounts while learning the ropes. If you are shooting to be a Multi-Million Dollar Practice you should consider getting your series 65 license.

A great feature available to taking over accounts of other adivsor's is the ACAT transfer which simply transfers the existing assets to your care where you can then allocate to desired funds. No need to liquidate an account and send a check. No need to bother with former advisors.

Advisory Platforms / Clearning Firms Available at IP¶

Visit our "IP Advisory" folder in Proton Drive for brochures, data sheets and much more information.

In addition to the below, we have numerous other TAMPs such as Assetmark, Eqis, Dunham, Hanlon, LVZ, etc.

Tabs¶

Assetmark¶

- 0.25%

AXOS Clearing¶

- Platform fee:

0.10% - Fees example:

- American Funds ICA (F2): 0.37%

- Advisor: 1% (Advisor can select between 0.25% - 3%)

- Total: 1.47%

- Account minimum: none

- You can select indidivual American Funds mutual funds (F-shares).

EQIS¶

Fee varies based on program (fully managed sub account starts at 1.00%, ETF Model programs 0.75% or ETF portfolios 0.48%).

Interactive Brokers¶

0.10% advisor managed, fully electronic, requires tech savvy advisor and clients. Focused for use by technical traders.

Orion Portfolio Solutions (OPS)¶

TAMP with varying fees based on allocated programs/models. Starts at 0.28% for accounts <100k managed by advisor

Pontera¶

0.30% in-force client 401k management platform, requires additional RIA account to bill from.

RBC¶

0.10% all accounts directed/traded by IAR. Can use an integrated platform for models/portfolios (Envestnet) which has breakpoint + portfolio manager fees (ex. 0.20% and up)

Securitize/Anchorage Digital¶

- Crypto Currency trading platform

US Bank¶

- $500 annually, accounts over $1 million switch to 0.05%

¶

Additional Info About our Advisory Platform¶

-

The general minimum our firm observes is $25,000 for an account. It does not mean an account will be rejected, but a principal may communicate with the advisor as to why a smaller account is opening on the fee side.

-

You can charge per plan, and even per hour. See page 13 of 16 on our contract for planning fee parameters.

-

Financial planning software: Most, if not all, the “mainstream” planning software services are approved for use. They are purchased/subscribed by the IARs themselves and retained as their own program. I could not advise on the costs of each as the providers typically use a tier-based system depending on what the advisor is looking for. We have a data package that is called RBC Black. It includes CirclBlack, a reporting software like DST vision (geared towards BD/RR business), Redtail, Nitrogen (Riskalyze), and MoneyGuidePro. The RBC Black package is $180 per month.

Notable Investments¶

Capital Group Separately Managed Accounts¶

The Active Core Portfolios are underpinned by mutual funds from American Funds. These funds have a high manager ownership and low expense ratios.

-

Mission statement: Protect and then grow it.

-

A unique feature of the Capital Group Separately Managed Accounts is that the client actually sees the individual stocks that have been purchased on their behalf. T

- The Capital Group also has a feature that pays attention to tax efficiency holding or selling to maximize not only profits but tax advantages.

- Customizations, maximum 10% change. filter-out stocks you don't want. he client can also make social cause changes to a certain extent and still stay in the general fund group.

- SMA were built for CG's own friend's and family 40 years ago. And they have a lot of their own money in them.

- Conversation: downside is lower than benchmarks and lower beta.

- Tax-aware. constrain portfolio to 25 - 30% turnover.

- Small amount of issues. highly concentrated.

- Annual management fees:

- Global Gowth SMA: 0.45%,

- US Equity SMA: 0.40%

- US Core SMA: 0.40%

A-Share vs Fee-Based¶

Watch A-Share vs Fee-Based Overview (2023-08) VIDEO

Read Edward Jones Sued By Clients Who Were Switched To Fee-Based Accounts (2018 April) ARTICLE

Ask Nick Murray...¶

QUESTION FROM AN ADVISOR¶

- Adapted from NMI 2001-05.

Do you have an opinion on whether managed accounts are generally considered better for investors than traditional open-end mutual funds?

I’m assuming a minimum of $100,000.

NICK MURRAY'S ANSWER¶

My personal judgment is that, ALWAYS ASSUMING SIMILAR COSTS, the upside of managed accounts is the potential for sharper focus, and for greater tax-efficiency (for non-qualified accounts). The downside is the difficulty of achieving sufficient diversification.

As a general rule, I’d say that if you haven’t got $500,000 (assuming $100,000 minimums) to spread over five very differently managed equity accounts, then stick with mutual funds (especially in tax-deferred accounts).

And even five separate accounts may not have more than 100-120 stocks among them, which may or may not be enough to provide truly meaningful diversification.

Cost Comparison of A-Share vs F3-Share¶

Pro-Tip: use the American Funds Share Class Cost Comparison Calculator to run your own comparisons.

- $10,000 initial investment.

- A-share is with no breakpoint: 5.75%

- F3 share (cheapest) + 1% Advisory share (I forgot to add the platform fee. 0.1% is one of the lowest)

- Fund: ICA

- Within 72 months the A-Share is cheaper for the client.

- This is with the "worst" A-share and the "best" Advisory share-class.

Growth Comparison of A-Share vs F3-Share¶

- I ran the illustrations below with American Funds' Hypothetical Tool using a real fund with real historical performance. The results shown are ending account balances net of all fees.

- Fund: Growth fund of America

- 10 year time-frame: 8/1/2013 – 7/31/2023

- A-shares are at all available breakpoints. At $1M there is no upfront sales charge.

- All examples include $6,500 annual contributions.

- F3 shares, which are the cheapest, are with a 1% advisor fee. (I forgot to add the platform fee. 0.1% is one of the lowest)

| Initial Amount | A UFSC | A Result | F3 Result |

|---|---|---|---|

| $10,000 | 5.75% | $121,667 | $121,834 |

| $25,000 | 5.0% | $175,461 | $173,742 |

| $50,000 | 4.5% | $252,579 | $247,428 |

| $100,000 | 3.5% | $408,655 | $394,801 |

| $250,000 | 2.5% | $879,310 | $836,919 |

| $500,000 | 2.0% | $1,665,935 | $1,573,782 |

| $750,000 | 1.5% | $2,459,728 | $2,310,645 |

| $1,000,000 | 0% | $3,293,510 | $3,047,508 |

A-share"Hidden Fees"?¶

Watch AF MKOM 1683 - Ideal Client VIDEO

I have an Advisor friend at another company with whom I've been talking withh for a long time. A few years ago he mentioned that A-share, retail mutual funds have "hidden fees" in addition to the upfront sales charge and annual expense ratio (this came up in a discussion in reference to fee-based and SMAs).

I had never heard of this from anyone else, even from fee-based proponents. But, I spoke with him a few days ago and this topic came up again, so I decided to call American Funds directly and also run the commissions calculator on American Funds website, which is approved for the public.

American Funds assured me that other than the upfront-sales-charge and the expense ratio there are no other fees.

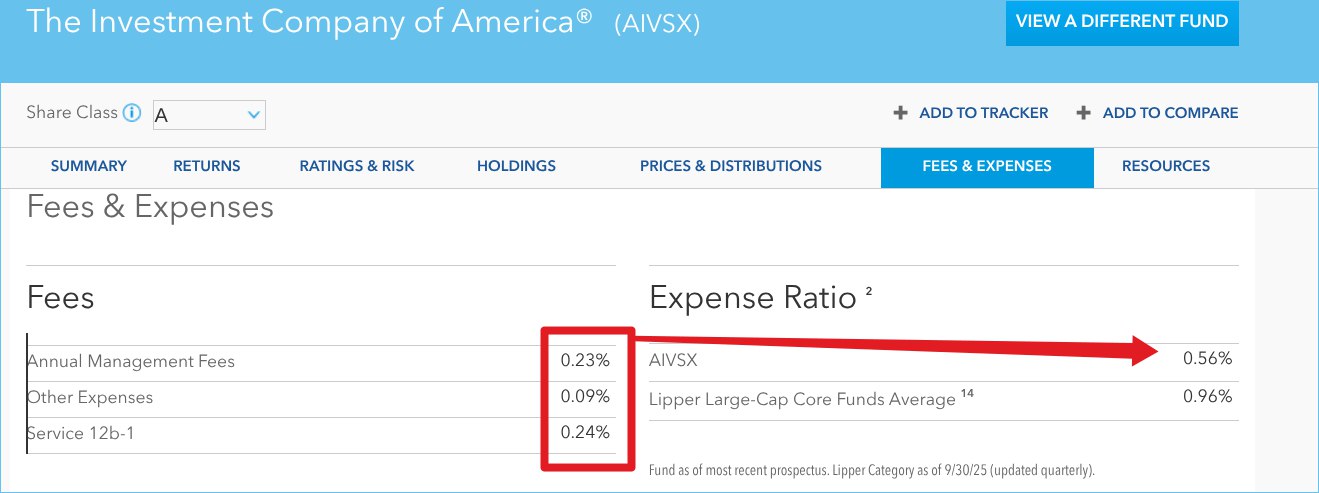

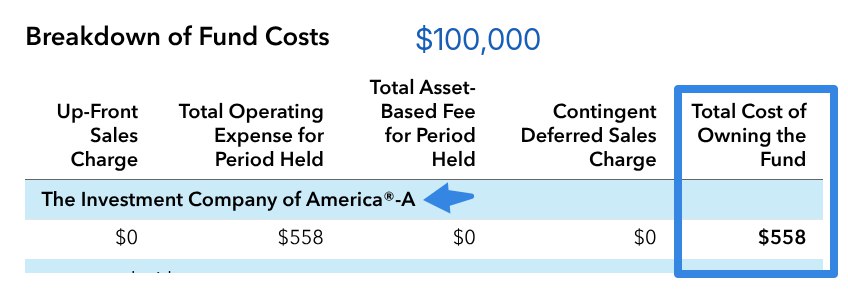

Example Using the ICA¶

- The Investment Company of America's total fees to the client 0.558%. Period.

In the cost calculator I put in the ICA with a 0% rate-of-return and it should decrease the fund value by the total cost, including any hidden fees. As you can see, the total cost is $558 on $100,000 balance which is exactly the 0.558% expense ratio.

Note: all published rates-of-return by A/C shares always include all sales charge, include the upfront-cost. The % is the NET to the client.

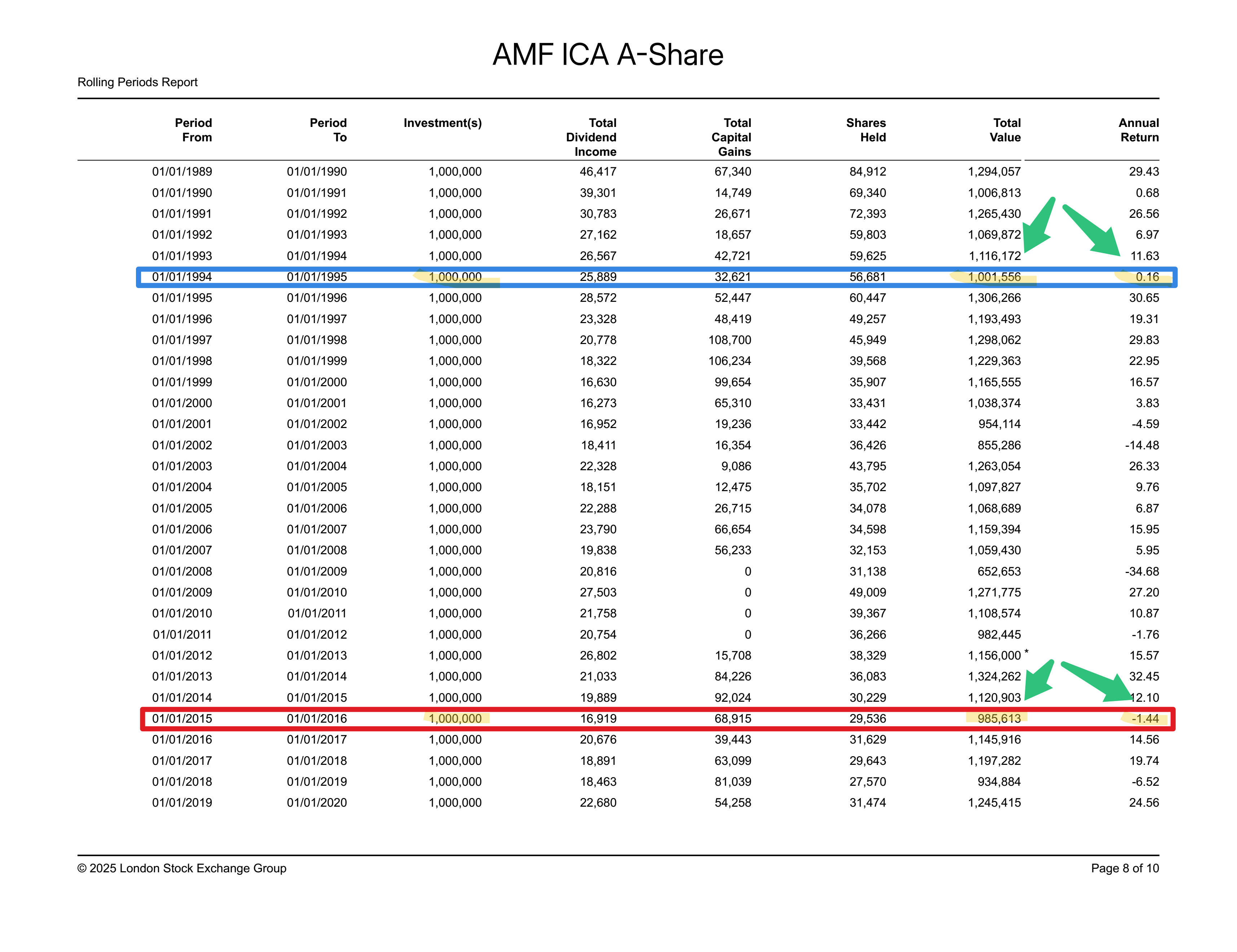

All Fees Are Included in the ROR¶

An important note to make is that the expense ratio (which is the totality of all fees) is already reflected in the rate-of-return and doesn't come out of the client's account (as fee-based fees DO).

To demonstrate this I ran a hypo for every year of the ICA from 1934 to present. I wanted to find a 0-percent year because it would be easiest to see, but there isn't one, so I found the two closest returns to zero - one slightly over and one slightly less.

If you look at the table you'll see that the $1,000,000 account balance at the beginning of the year adjust by the end of the year by EXACTLY the stated rate-of-return. Meaning, all fees are ALREADY included.

By way of comparison, if a fee-based/advisory invest states a rate-of-return is does include the management fees, but it does NOT include the platform fee, the advisory-firm fee (if there is one) nor the Advisor's fee.

Fiduciary?¶

For more about this "issue" visit AFW 1.12.4.

CFP?¶

Question from an Advisor: "It seems like nobody gets the blood, sweat, and tears I put myself through to get the CFP. No prospects or clients seem to even know what it is."

Oh, financial advisors.

(sigh)

Why on earth would they care enough to be curious to dig around about YOUR licenses?

It's always about THEM - not YOU, people!