“Lies, damned lies, and statistics.” ―Benjamin Disraeli

Watch Deption of the Rate-of-Return VIDEO

Watch AF MKOM 1666 - Deception of Rate-Of-Return & Fallacy of the Hypothetical VIDEO

Average Rate-Of-Return and Volatility¶

-

Long-term average rates-of-return are important.

-

However, if the rates-of-return are similar in two mutual funds, then the one with lower volatility may be a better choice, as it doesn't have to "work as hard" to maintain its average. And reduce the psychological stress of the client.

-

This concept applies to fees/annual expenses, as well.

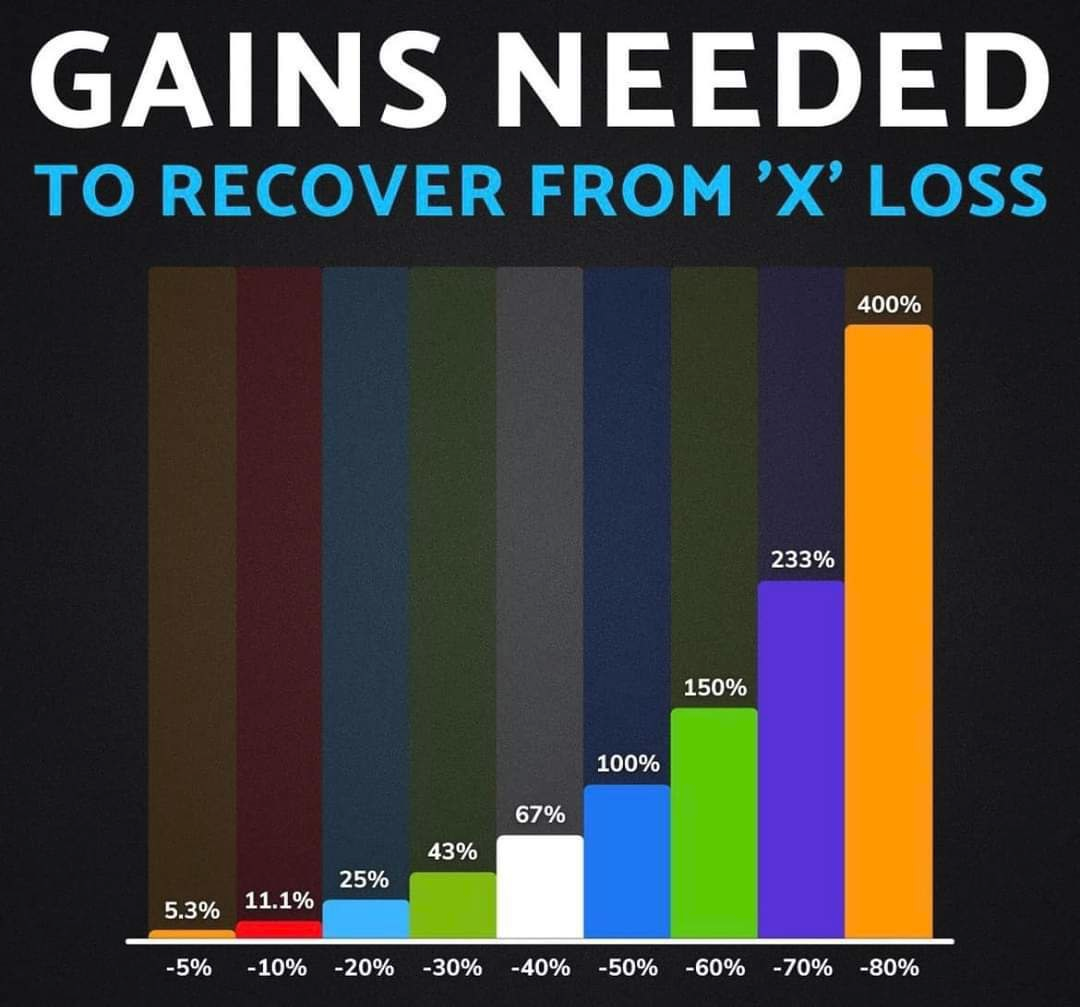

Example 1¶

- Year 1: Invest $100,000

- Year 2: Lose -50% (new balance is $50,000)

-

Year 3: How much return do you need the get back to your original $100,000?

-

Answer: You need $100%! (not 50%)

Example 2¶

Fallacy of the Hypothetical¶

Please do not let the title of this principle mislead you. Hypotheticals are one of the most powerful tools you have in your arsenal. Often however, proponents of fixed-accounts will use a negative history to "demonstrate" that the stock market is volatile or doesn't perform well. This is wrong.

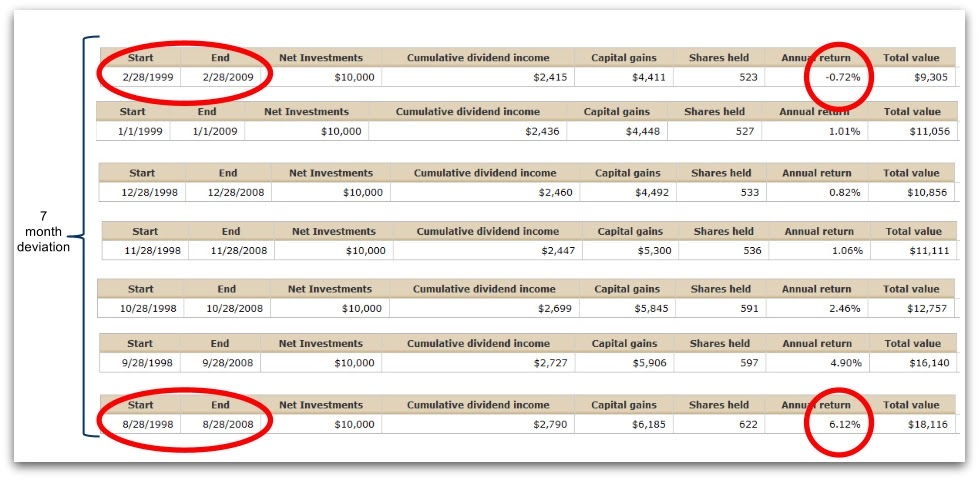

Start/End Date Deviation¶

When running a hypothetical, especially one that initially appears to have a low return, check the Start/End Date Deviation.

For a more accurate historical performance run all available "rolling-periods". And show the median of all those periods.

From the above statistic one could infer that the ICA has been a poor investment for the last 10 years. And that investing within the last 10 years would yield a negative return, and it wouldn't be worth it at all.

Not so fast...

The hypo only compares two days (Feb 28 1998, and Feb 28 2008) out 3,650 days! The other 3,648 days in between are ignored.

Changing the Start/End dates by just seven months, improves the 10-year average by +6.84%, from -0.72% to 6.12%!

A Tool to Handle Objections¶

You can use this principle to handle objections. For example, if someone states that the last 10 years the market has been poor, your response could be...

Well, it depends how you run the numbers. We call it Start/End Date Deviation. For example, if you analyze one of our mutual funds, the ICA, from Feb 1998 to Feb 2008 the average return is -0.72%. But if you shift the dates just 7 months, from Aug 1998 to Aug 2008, then the 10-year average return is 6.12%.

A 7 month deviation made almost a 7% difference over 10 years!

Read Nick's NMS 17 - The mindless tyranny of benchmarks PDF