title: Minor Tax Shelters & Accounts description: [AFW S.3.2] 529-Plans, Coverdells, UTMA/UGMA, TRUMP Accounts, ABLE Accounts published: true date: 2026-06-30T08:09:01.401Z tags: editor: markdown dateCreated: 2021-05-24T23:14:38.096Z

Overview¶

Watch Granda's $100k for Grandchild VIDEO

529 Plans¶

Read Expand your practice with 529 education savings plans by Capitla Group ARTICLE

Read 529-Plan Myths & Facts PDF (thanks to Dave McDanal)

Watch 529 Plan Myths by David MccDanal, part 1 VIDEO

Watch 529 Plan Myths by David MccDanal, part 2 VIDEO

Moving 529-Plan to Roth IRA¶

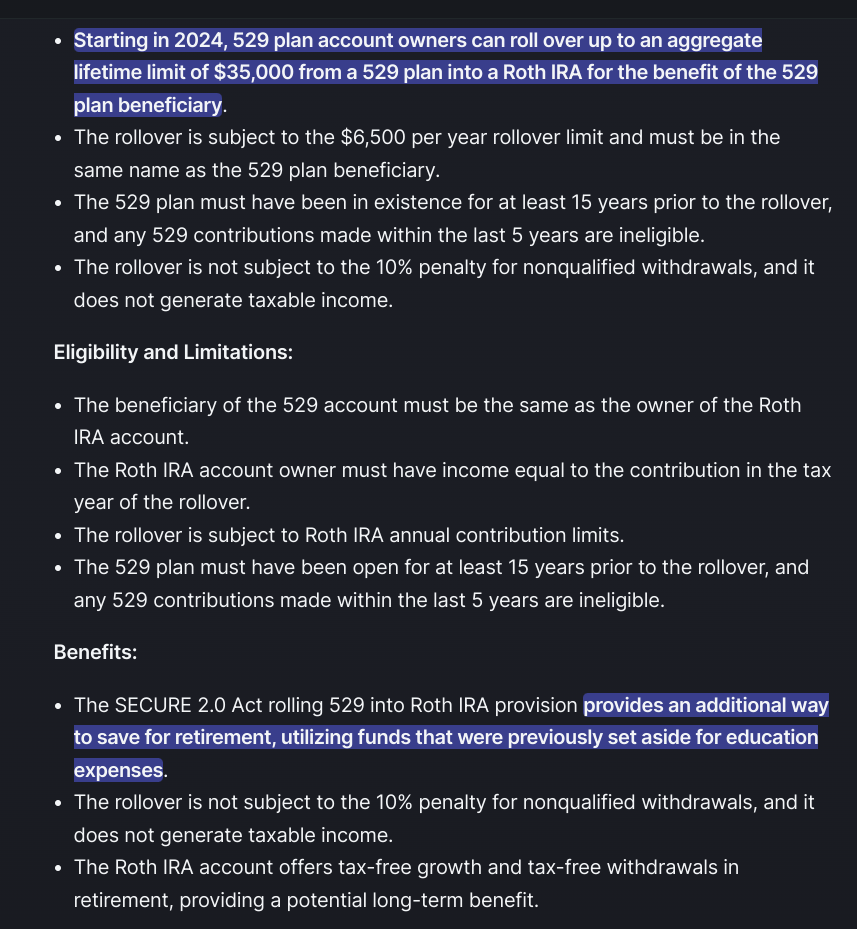

SECURE 2.0 Act of 2023 allows you to move money from a 529 to a Roth IRA after 15 years, subject to annual Roth contribution limits and an aggregate lifetime limit of $35,000. Rollovers cannot exceed the aggregate before the 5-year period ending on the date of the distribution. The rollover is treated as a contribution towards the annual Roth IRA contribution limit.

March 2022 Update¶

Effective for the 2024/2025 school year, distributions from a grandparent-owned 529 account will no longer affect financial aid.

What’s more, since FAFSA uses income from two years back to determine eligibility, that means that grandparent-owned 529 accounts won’t affect aid calculations beginning this year.

Starting in the 2024/2025 school year, qualified distributions from a grandparent-owned 529 account will no longer be reported as untaxed income to the beneficiary. And since the Free Application for Federal Student Aid (FAFSA) uses income from two years prior to determine aid eligibility, grandparent-owned 529 accounts will no longer affect financial aid beginning in 2022.

Previously, any qualified distribution from a 529 plan owned by a grandparent for the benefit of a grandchild counted as untaxed income to the beneficiary. There were a number of strategies to mitigate it, including holding off on using distributions from the 529 until the student is in the second semester of his or her sophomore (if graduating in four years) or junior (if graduating in five) year.

Now grandparents can open and maintain a 529 without worrying about FAFSA eligibility.

Aggregate limits¶

Note: the limit for the AMF CollegeAmerica 529 savings plan has been increased to $550,000.

Unlike IRAs or 401(k)s, there are no annual contribution limits for 529 plans. However, there are maximum aggregate limits, which vary by plan. Under federal law, 529 plan balances cannot exceed the expected cost of the beneficiary's qualified higher education expenses. Limits vary by state, ranging from $235,000 to $550,000. This amount represents what the state believes to be the full cost of attending an expensive school and graduate school, including textbooks and room and board. If your plan is close to the limit don't worry about future earnings in the account pushing it over. The funds can remain in the account without penalty, but the family will not be able to make any future contributions unless a market drop brings the account balance back down.

529-to-Roth¶

If not used for college expenses, a 529 Plan can be converted to a Roth IRA! However, there are limitations to protect the integrity of 529s as education savings accounts and deter individuals from using them as wealth-transfer tools.

-

The 529 plan of a designated beneficiary must be at least 15 years old.

-

The Roth IRA needs to be in the name of the beneficiary.

-

The rollover amount cannot exceed the aggregate amount contributed to the program (including earnings) before the five years ending on the rollover date.

-

Rollover contributions must be within IRA annual contribution limits, which would include any other IRA contributions made by the beneficiary in that year.

-

The income limitations for regular Roth IRA contributions do not apply to 529-to-Roth rollovers; however, the beneficiary will be required to have a certain level of earned income.

Gift Tax¶

Individuals can defer up to $80,000 in a tax-deferred account to pay for a child’s education without incurring a federal gift tax. Normally, an individual can give another individual only $16,000 a year without incurring gift taxes. Under IRC Section 529, however, an individual can use up to 5 years of annual $16,000 exemptions at once when contributing to a child’s post-secondary education.

Couples can defer up to $160,000 in a 529 account to pay for each child’s education. The IRS considers a lump sum $80,000 gift to one of these plans the equivalent of five $16,000 gifts made over a 5-year period. A single gift of $80,000 can qualify as 5 years’ worth of gift tax exclusions as long as, no additional gifts are made to the beneficiary over the 5-year period and the donor lives 5 years. That is the largest amount that can be transferred without triggering a taxable gift in a single year.

American Funds CollegeAmerica 529-Plan (Virginia)¶

- American Funds CollegeAmerica web page

- $500,000 maximum contribution limit per beneficiary.

- Launched in 2002.

- Chosen by more than 110,000 advisors and more than 1 Million families nationwide.

- The country’s largest plan, with assets topping $65 billion.

Running a AMF 529-Plan Calculation Illustration¶

Watch AF MKOM 1658 - Creating report for 529 plans VIDEO

Watch How to run an 529-Plan Illustration with American Funds' software VIDEO

American Funds College Target Date Series¶

Seven target date funds were designed to address the key challenges of saving for the rising cost of education. A single investment provides diversification and a glide path matched to each client’s investing time horizon, making saving for education easier than ever.

Coverdell Accounts¶

Advantage for Coverdell is that it can be used for costs of school K-12 and college.

The bummer is that only $2000 can be put in for each child subject to your own income limits. (You can always gift the $ to the child & have them open the account.)

Disadvantage is that $2000 is the limit. If grandma wants to contribute & you go over the limit there is a 6% excise tax. Other disadvantage is that the Coverdell is not revocable like a 529. At age 30 the account must be distributed to the beneficiary who will pay a 10% penalty on the growth and tax. The beneficiary can be changed to someone in the same family.

The 529 is better overall for accumulation of $. See +Michael Thomas example recently where there was a lump sum put in to the 529 which very nicely reached the client goal. Comments by +Michael Thomas were also insightful. They all have to be used for education however I always use the opportunity cost of deciding if an alternative use of the funds would justify the tax and penalty, then let the client make the decision.

ABLE Accounts¶

Watch Overview of ABLE accounts 1 VIDEO

Watch Overview of ABLE accounts 2 VIDEO

Listen to ABLE Accounts - Making Special Needs Planning a part of your practice - Capital Group podcast - June 2025 AUDIO

For brochure and info PDFs and videos visit the ABLE folder PROTON DRIVE

Read What type of disabilities qualify for an ABLE Account? ARTICLE

Read FINRA's ABLE Accounts (529-A Savings Plans) ARTICLE

For families caring for individuals with special needs, the questions can be daunting.

Among the 53 million Americans providing unpaid care for loved ones, 62% of them feel overwhelmed by financial stress. A significant contributor to that stress: lack of planning. Only 15% created a caregiving plan ahead of time. And even among those who did make a plan, only three in ten included financial needs beyond caregiving, and just over two in ten included legal documents like wills and powers of attorney.

Investment account available to individuals with mild to severe disabilities. Achieving a Better Life Experience (ABLE) Act was signed into law in 2014. Individuals can save up to $16,000 per calendar year (2022). They can have up to $100,000 in the account without the amount being counted against the $2,000 limit on personal assets to qualify for SSI. Savings grow federally tax free (and maybe state tax free) if used for qualified disability expenses. Money can be withdrawn tax-free to pay for qualified disability expenses.

Deepen relationships and do planning with entire families You may already have special needs planning opportunities in your existing book of business. “The belief that it doesn’t apply to you is a misjudgment on an advisor’s part. The prevalence of disability today is frankly staggering,” Norton insists. “One in 31 children in the U.S. is considered to be on the autism spectrum. That’s the CDC’s number.” In fact, the prevalence of autism is on the rise, as shown by a CDC study of over 8,000 children (eight years old) in 2022.2

Because disability doesn’t only change the life of one person but also the lives of their loved ones, special needs planning involves planning for entire families. The financial stability of the caregiver can be just as important as that of the special needs individual.

“I’ve had situations where I’ve set up a special needs account … and then we’ve had $800,000, $900,000 rollovers of retirement plans because when we do our planning for these families, we’re doing it in context of not only the special needs individual, but the other family members that are supporting that special needs individual,” Norton says. “Mom and dad need to have their house in order … because if their finances are a mess, they certainly won’t be in a position to help the special needs family member.”

Disability also creates risk management needs. “Life insurance is an important tool in the special needs planning toolbox,” Norton notes. “Particularly, second-to-die policies for couples that will fund a special needs trust.”

An advisor who offers special needs planning can be an oasis in the desert for families affected by disability. Thinking back to when his own son was diagnosed, Norton recalls, “I remember back then feeling somewhat lost, and at times, had a sense of hopelessness about the situation. It was really, truly overwhelming.” From personal experience, he tells advisors, “Having empathy for that situation, for those clients, can cement your relationship with them.”

That’s why Norton makes sure he broaches the topic at the earliest opportunity. “I make it part of the regular intake that we do when we sit down with folks for the first time,” he says. “You should be asking the question, ‘Do you have someone that is dependent on you financially, that has special needs?’”

In Norton’s view, advisors benefit from the fact that there isn’t as much stigma about special needs as there used to be. “People are pretty open … more so than they maybe had been historically. So, it just kind of comes up in conversation.”

Master ABLE accounts as your entry point If you’re making your first foray into special needs planning, Norton recommends starting with ABLE accounts. “Think of them as a first step for families,” he suggests.

Established by the ABLE Act of 2014, ABLE accounts are tax-advantaged investment accounts for people with disabilities. “ABLE accounts allow individuals to save money while protecting benefits that otherwise might be put in jeopardy if they had too many assets in their name,” Norton explains. Tax-advantaged treatment applies to savings used for qualified disability expenses. State tax treatment varies.

To qualify for an ABLE account, individuals must have had a physical or mental disability that began before age 26. On January 1, 2026, the limit is changing from 26 to 46 years old. “That’s going to greatly increase those who are eligible to use ABLE accounts,” Norton notes.

In 2025, the annual contribution limit is $19,000. Some qualified ABLE account holders can also contribute an additional $15,650, which means they can have a total maximum annual contribution limit of $34,650.

ABLE accounts also have flexible distribution rules. Norton explains, “There are two tests to determine if something is a QDE [qualified disability expense]. Does it relate to the individual’s disability? And then more broadly speaking, does it maintain or improve health? Does it provide for independence or improve quality of life? So these criteria are intentionally broad.”

If withdrawals are used for purposes other than qualified disability expenses, the earnings will be subject to a 10% federal tax penalty in addition to federal and, if applicable, state income tax.

Build knowledge and strategic partnerships For advisors who want to offer special needs planning, Norton recommends a few specific action steps.

On the professional development front, Norton notes that the ChSNC designation is currently the only designation focused specifically on special needs planning. The coursework can be completed in under a year, according to The American College. Norton also recommends joining the Academy of Special Needs Planners, a large and active network of planners, advisors and trust officers.

Norton also encourages getting involved with the disability community, especially through local organizations and nonprofits. “Become part of it,” he says. “Volunteering with those nonprofits, getting known within the community, I think is important.”

Advisors who offer special needs planning should make sure that centers of influence (COIs) know about it. It helps to differentiate your practice. “If you approach that CPA [certified public accountant], ‘I’m a financial advisor, hi, my name is Steve. I can help your clients with investing and planning for their future, refer them to me,’ that doesn’t ring home as well as, ‘I have a focus on helping families that face special needs situations,’” Norton explains.

Whether or not you’ve been personally impacted by disability, Norton’s story demonstrates the value of special needs planning for all financial advisors. It helps you stand out to prospects and COIs. It allows you to deepen your relationships with entire families. Most importantly, it enables you to meet the needs of a historically underserved population in profound, life-changing ways.

Who is Eligible?

- U.S. Citizens and permanent residents who can legally own securities, including individuals who are blind or disabled from a condition that began prior to age 26.

- Those who meet the age requirement and may be eligible for SSI or SSDI benefits because of their disability.

- Individuals with a written, signed diagnosis form a licensed physician. (This does NOT need to be submitted to AMF. Client just needs for own records).

Who Owns the Account?

- The beneficiary

Examples of Qualified Disability Expenses (QDEs)

- Basic Living Expenses

- Health and Wellness

- Housing

- Financial Management

- Transportation

- Education and Training

- Assistive Technology

- Legal Fees

- Profession Services

American Funds ABLE America

- Nation’s only advisor-sold ABLE account

- A shares only

- AMF portfolios only

Additional Information Needed for Application

- Account Owner info (individual with disability)

- Authorized Representative (legal guardian)

- If account owner is over 18 and has a court-appointed legal guardian - important things to know about guardianship/conservatorship

- Must send a copy of Guardianship court order

- Guardianship paperwork should be recent (within the last 60 days). Because of the coronavirus shelter-in-place orders, AMF is making exceptions to this. If the guardianship paperwork is older than 60 days, they will call the court and confirm that the order is still in good order. However, AMF has required one of my clients to get an updated order before all the virus shutdowns in order to open the account.

- Conservator includes all financial authority. If Authorized Representative is the conservator (and states “conservator” on paperwork) then this includes the power to make financial decisions.

- Guardianship paperwork needs to explicitly state that the guardian has authority to make financial decisions on behalf of the individual with the disability. “Full Guardianship” does not necessarily mean they have financial authority. It needs to say “financial” somewhere on the document. This is very important.

- If the guardian is a government entity, you must submit an Entity Beneficial Owners (for Intermediaries) AMF form. You must also include a signed and dated letter (less than 60 days old) stating the person(s) at the entity who have authority to act on the behalf of the disabled individual.

- If the individual has multiple guardians, only one is required to be the “Authorized Representative” on the paperwork unless guardianship order states that the guardians must act together. In that case, you would need to put both guardians down as co-Authorized Representatives and they would both need to sign the paperwork.

- Basis for ABLE Account Eligibility (disability must have occurred before age 26)

- SSDI

- SSI

- Physician’s diagnosis and signed letter, permanent disability

- Account Owner’s Disability Type

- Developmental Disorder

- Intellectual Disability

- Psychiatric Disorder

- Nervous Disorder

- Congenital Anomaly

- Respiratory Disorder

- Other

Important Note: If owner dies, ABLE account is subject to Medicaid payback

Advisor Benefits for ABLE Opening ABLE accounts

- No competition

- Special Needs community - well connected and extremely active. They will spread the word. Reach out to special needs groups in your community and they will reach out to their members with your info

- Support services - there are many special needs support providers who have many clients that need ABLE accounts. Reach out to these support providers and let them know what you’re doing.

- Many clients need ABLE accounts quickly. They might be over the allowed $2,000 and need the account created fast in order to keep their benefits. You have the ability to be efficient and get the account established and funded in a timely manner.

- You become the family’s financial advisor

- If they are happy with your work, they will tell others in the special needs community

- Great opportunity, especially for newer advisors

- Reach out to estate planning attorneys

- Present a seminar on ABLE accounts and special needs trusts. This was my most well-attended seminar (around 30 people came). I gained 5 new clients from that meeting and have several more meetings scheduled from that one seminar.

UTMA/UGMA¶

Uniform Gifts to Minors Act (UGMA) or Uniform Transfers to Minors Act (UTMA) accounts.

Read Investopedia: UTMA ARTICLE

Guidelines for Uniform Transfers to Minors Act (UTMA) accounts allow minors to receive gifts or transfers of money or securities. Any money or securities given to a child are irrevocable gifts. A custodian must be listed in the registration of the account (you or your mom) to act on behalf of the minor until the child reaches the UGMA/UTMA age of majority (18 in CA). When the child reaches the age of majority, the child is entitled to the account.

Anyone can contribute to an UGMA/UTMA account and there are no income limits.

You can give up to \(15,000 per child each year free of gift tax consequences (\)30,000 for married couples). Contributions are made with after-tax dollars, so a deduction for the contribution cannot be taken.

Even though the minor becomes the owner of the account at age 18, the custodian still retains control of the account. In order for the new owner to get control of the funds, he/she would have to open an account and the custodian would have to have the funds transferred to the new account.

Contributing to UGMA/UTMA¶

Grandparents, siblings and other family members can contribute to UGMA accounts. For example, if someone wants to contribute to an American Funds account, do the following:

1. Send a check payable to American Funds.

2. Include a note:

This check is for a UTMA/UGMA account:

- Account #:

- Minor child:

- Please invest in the same allocations as the account is already set-up as.

3. Mail to: American Funds, 12711 N. Meridian St 9181, Carmel, IN 46032

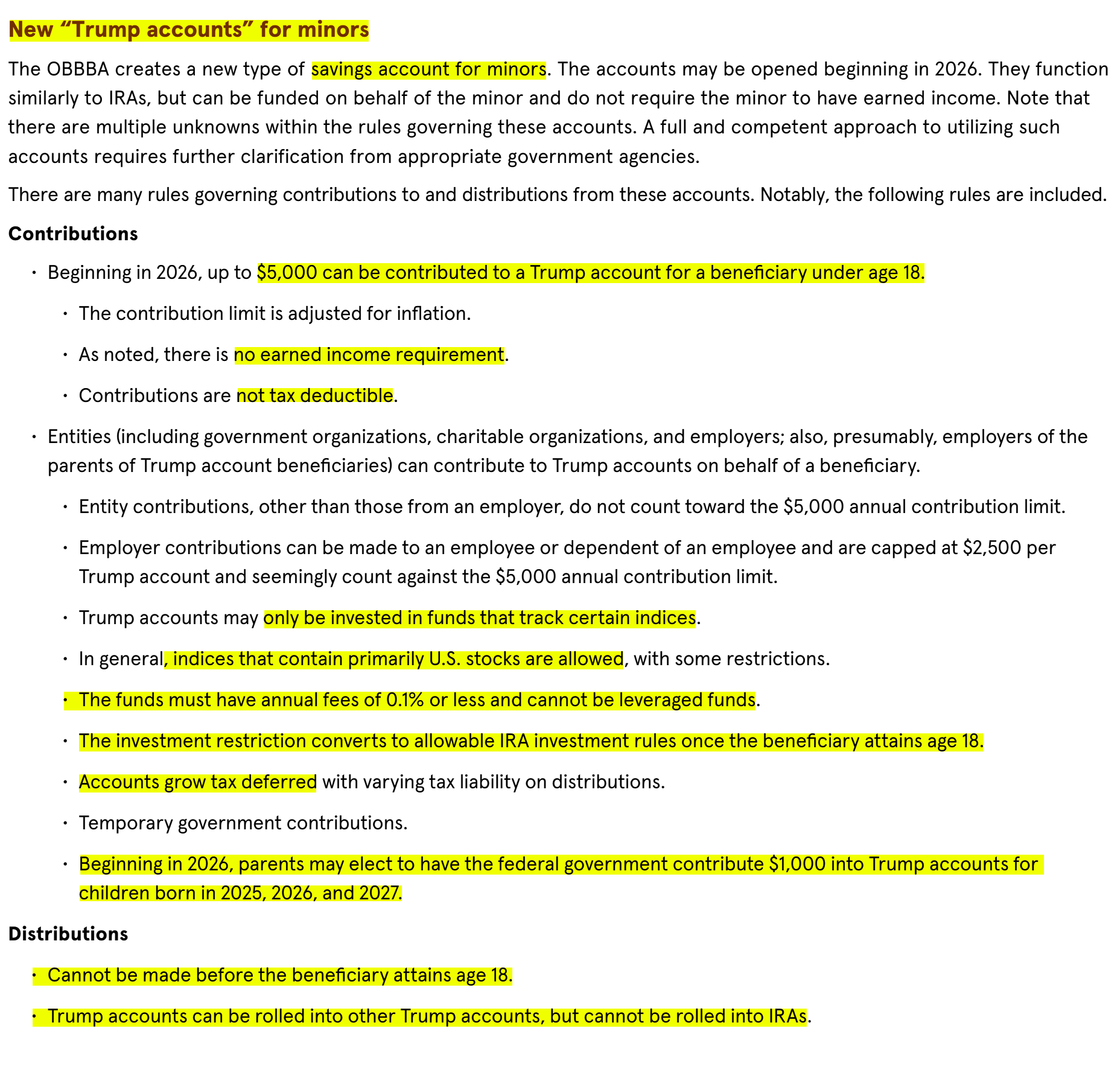

TRUMP Accounts¶

Variable Annuity for Retirement¶

Gift Tax¶

Read What Is the 2022 Gift Tax Limit? ARTICLE

Pro-Tips¶

UTMA or 529-Plan?¶

When choosing between a UTMA and a 529-Plan for saving for children's future, there are many considerations. However as a general rule-of-thumb put the first $16,000 - $22,000 into an UTMA, and the remainder into a 529-Plan.

The primary benefit of a 529-Plan is the tax-free withdrawals, but the drawback is that the funds have to be used for higher-expenses.

An UTMA, on the other hand, allows the child to use the money for any purpose (at the age of majority), but the drawback is its not tax-free. However, the first $1,100 of earnings are tax-exempt, and the next $1,100 is taxed at the child’s rate (which is probably in the 10% - 12% tax bracket), and any income over $2,220 is taxed at the parent’s rate.

So, if we assume the mutual funds earn 10%, it makes sense to put the first \(22k into a UTMA because the taxes on the earnings will be either zero or very low, and the monies can be used for any purpose. But, in order to avoid the **gift tax** we’ll make this limit **\)16,000** (single “giver”) or $22,000 (married “givers”).